Summary: Private capital expenditures down again, less than expected; fall smaller than in June quarter; equipment investment “key source of surprise”; 2020/21 capex estimate 6.3% higher than previous estimate, lower than comparable estimates from 2019/20; non-mining firms upgrade investment plans “substantially”, mining firms make reduction; business investment to “detract from private demand recovery.”

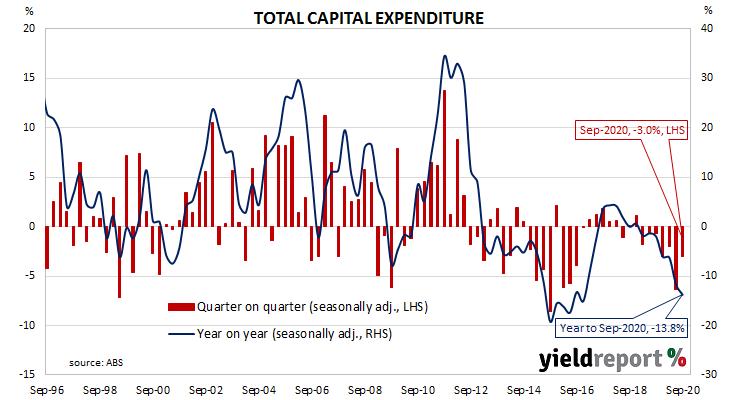

Australia’s capital expenditure (capex) slump was thought to be coming to an end as investment in the mining sector reverted back to its long-term mean after a spike early in the decade. Total investment had begun to grow again, driven by investment in the services sector. However, quarterly contractions have become the norm through 2019 and 2020.

According to the latest ABS figures, seasonally-adjusted private sector capex in the September quarter fell by 3.0%. This latest figure was less than the 1.5% contraction which had been expected but higher than the June quarter’s revised figure of -6.4%. On a year-on-year basis, total capex contracted by 13.8% after recording an annual rate of -11.7% in the previous quarter after revisions.

Westpac senior economist Andrew Hanlan said the change in equipment investment “was the key source of surprise…”

Long-term Commonwealth Government bond yields fell a little on the day. By the close of business, the 10-year Treasury bond yield had lost 2bps to 0.91% and the 20-year yield had slipped 1bp to 1.55%. The 3-year yield remained unchanged at 0.17%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.05%, remained unchanged. At the end of the day, contract prices implied the cash rate would slip a touch closer to zero in December and then settle at around 0.04% to 0.05% through 2021.