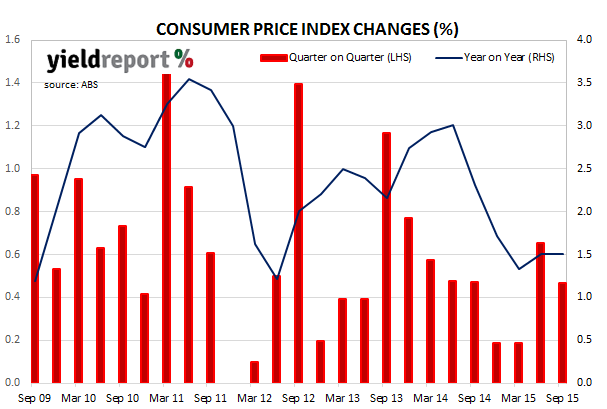

The September quarter CPI figures surprised markets by coming in well below expectations at +0.5% and +1.5% for the year to the end of September. The market expected a +0.7% rise for the quarter and a +1.7% rise year on year. The underlying inflation figure, which strips out the more variable components of the measure, was expected to come in at +0.6% for the quarter and +2.5% for the year and have come in at +0.3% (q/q) and +2.1% (y/y).

Markets immediately saw room for the RBA to cut rates at its 3 November meeting with underlying inflation at the bottom of its targeted range. The dollar fell sharply and cash markets doubled the chances of a November rate cut, now pricing it as a 60% chance.

ANZ said the figures would not trigger a rate cut but nor would it stop the RBA should they decide to reduce rates. Shane Oliver, from AMP, said any inflationary effects from a lower exchange rate was being “swamped” and “there’s no barrier” to a rate cut on Cup Day. He fully expects the RBA to cut next week.

The breakdown of figures are as follows:

September quarter CPI: +0.5%

June quarter CPI: +0.7%

CPI to September year end: +1.5%

Underlying September quarter CPI: +0.3% (trimmed mean)

Underlying June quarter CPI: +0.6%

Underlying CPI to September year end: +2.1%