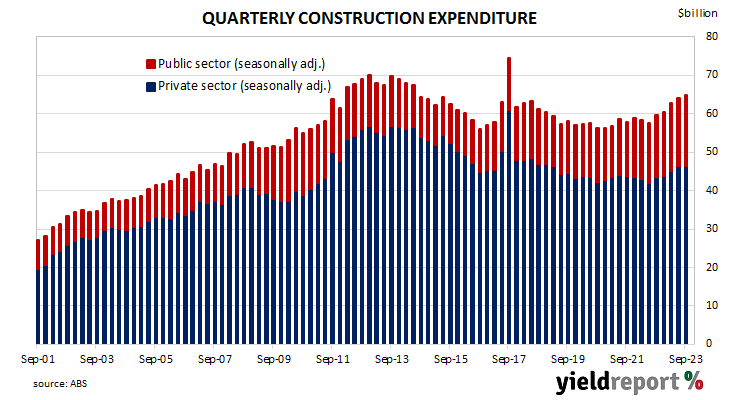

Summary: Construction spending up 1.3%, more than expected; Westpac: post mid-2022 activity burst continuing; Westpac: pace of growth set to fade in 2024; residential sector up 1.3%, non-residential building down -1.6%, engineering up 2.6%.

Construction expenditure increased substantially in Australia in the early part of last decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new projects and the expansion of existing ones to exploit a tripling in price of Australia’s mining exports in the previous decade.

According to the latest construction figures published by the ABS, total construction in the September quarter increased by 1.3% on a seasonally adjusted basis. The result was greater than the 0.5% increase which had been generally expected as well as the June quarter’s 2.0% increase after it was revised up. On an annual basis, the growth rate slowed from 11.0% to 8.5%.

“The Australian construction sector has experienced a burst of activity since mid-2022, supported by a strong pipeline of work and facilitated by an easing of supply headwinds and fewer disruptions,” said Westpac senior economist Andrew Hanlan. “As anticipated, that theme extended into the September quarter.”

The figures came out on the same day as the latest monthly inflation figures and Commonwealth Government bond yields fell significantly. By the close of business, the 3-year ACGB yield had shed 15bps to 4.02%, the 10-year yield had lost 14bps to 4.37% while the 20-year yield finished 12bps lower at 4.65%.

In the cash futures market, expectations regarding further rate rises softened considerably. At the end of the day, contracts implied the cash rate would remain close to the current rate of 4.32% and average 4.325% through December and January but then average 4.385% in February. May 2024 contracts implied a 4.415% average cash rate while August 2024 contracts implied 4.35%, 3bps more than the current rate.

“Looking ahead, the pace of growth is set to ease,” Hanlan added. “Notably, the level of construction work is now at or above the trend level of commencements across a number of segments. A sizeable work pipeline will sustain a high level of work but the pace of growth is set to fade moving into 2024.”

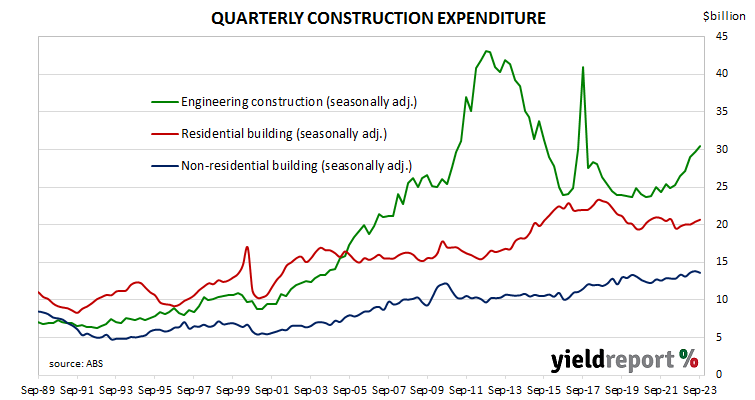

Residential building construction expenditures increased by 1.3%, less than the 1.8% rise in the September quarter after revisions. On an annual basis, expenditure in this segment was 4.4% higher than the September 2022 quarter, down from the June quarter’s comparable figure of 4.6%.

Non-residential building spending decreased by 1.6%, in contrast with from the previous quarter’s 1.3% increase. On an annual basis, expenditures were 1.9% higher than the September 2022 quarter, whereas the June quarter’s comparable figure was 7.6% after revisions.

Engineering construction increased by 2.6% in the quarter, a slightly larger increase than the 2.5% rise in the June quarter. On an annual basis, spending in this segment was 14.9% higher than the September 2022 quarter, down from the June quarter’s comparable figure of 17.8% after revisions.

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature, unlike unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.