Summary: US GDP down by 9.5% in June quarter; “terrible” but better than expected; “sharply lower” consumer spending; COVID-19 infections likely to slow recovery rate; GDP deflator drops.

US GDP growth slowed in the second quarter of 2019 before stabilising at about 0.5% per quarter. At the same time, US bond yields suggested future growth rates would be below trend. The US Fed agreed and it reduced its federal funds range three times in the second half of 2019 as a form of insurance against a softening economy. By the time pandemic restrictions were put in place in March, there was little left in the Fed’ armoury to soften the blow and fiscal measures were the only real option left.

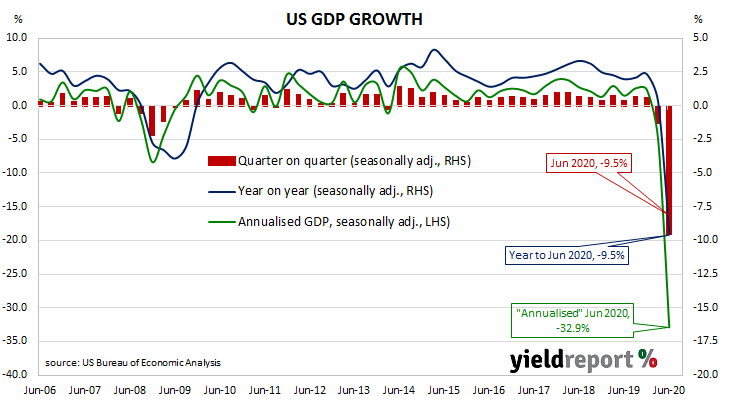

The US Commerce Department has just released June quarter “advance” GDP estimates and they indicate the US economy contracted by 9.5% for the quarter or at an annualised growth rate of 32.9%. The figure was slightly higher than the -9.9% (-34.0% annualised) which had been expected and it represented a marked deterioration from the March quarter’s final figure of 1.3%.

NAB Head of FX Strategy (FICC division) Ray Attrill described the result as “terrible, but not quite as bad as expected.”

“Unsurprisingly, the decline primarily occurred due to sharply lower consumer spending, particularly services which fell 13% (not annualised),” said Westpac senior economist Elliott Clarke.

US GDP numbers are published in a manner which is different to most other countries; quarterly figures are compounded to give an annualised figure. In countries such as Australia and the UK, an annual figure is calculated by taking the latest number and comparing it with the figure from the same period in the previous year. The diagram above shows US GDP once it has been expressed in the normal manner, as well as the annualised figure.

US Treasury bond yields fell by progressively larger amounts along the curve. By the end of the day, the 2-year Treasury bond yield had slipped 1bp to 0.12%, the 10-year yield had shed 2bps to 0.55% while the 30-year yield finished 3bps lower at 1.21%.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months retained a slight easing bias. OIS contracts for September implied an effective federal funds rate of 0.062%, about 4bps below the current spot rate.