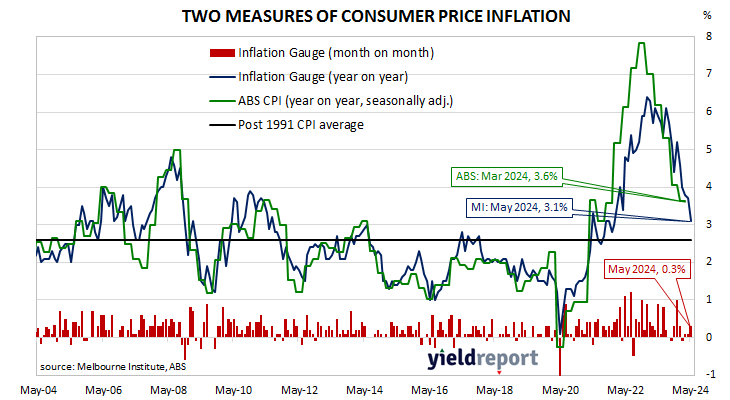

Summary: Melbourne Institute Inflation Gauge index up 0.3% in May; up 3.1% on annual basis; Westpac: could be sign of better inflation progress in May, too early to draw conclusions; ACGB yields fall; rate-cut expectations firm.

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate the ABS rate by around 0.1%, or at least until recently.

The Melbourne Institute’s latest reading of its Inflation Gauge index indicates consumer prices increased by 0.3% in May, up from the 0.1% increases posted in March and April. However, the index rose by 3.1% on an annual basis, down from April’s comparable figure of 3.7%.

“The inflation measure has tracked above the official ABS monthly and quarterly inflation results since the middle of last year,” said Westpac economist Jameson Coombs. “Taken alone this could be a sign we may see some better inflation progress in May. However, it’s too early to draw too much from the move.”

Commonwealth Government bond yields declined again, largely in line with falls of US Treasury yields on Friday night (AEST). By the close of business, the 3-year ACGB yield had lost 3bps to 4.02%, the 10-year yield had shed 4bps to 4.38% while the 20-year yield finished 3bps lower at 4.68%.

Expectations regarding rate cuts in the next twelve months firmed by the end of the day. In the cash futures market, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.315% through June and July and 4.345% in August. November contracts implied 4.335%, February 2025 contracts implied 4.285% while May 2025 contracts implied 4.18%, 14bps less than the current cash rate.

Central bankers desire a certain level of inflation which is “sufficiently low that it does not materially distort economic decisions in the community” but high enough so it does not constrain “a central bank’s ability to combat recessions.”