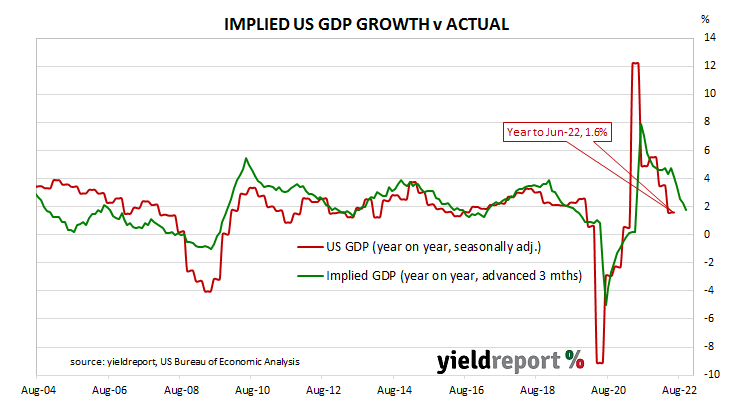

Summary: Conference Board leading index down 0.3% in August, lower than expected; index now down for six consecutive months; manufacturing sector work hours down, activity to “continue slowing more broadly throughout the US economy”; latest reading implies 1.8% US GDP growth to November.

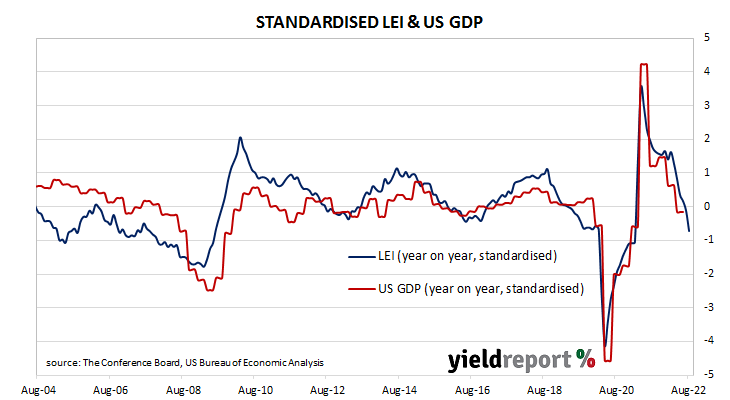

The Conference Board Leading Economic Index (LEI) is a composite index composed of ten sub-indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal growth peaks and troughs; turning points in the index have historically occurred prior to changes in aggregate economic activity. Readings from March and April of 2020 signalled “a deep US recession” while subsequent readings indicated the US economy would recover rapidly. More recent readings have trended lower, implying implied lower US GDP growth rates.

The latest reading of the LEI indicates it decreased by 0.3% in August. The result was lower than the 0.1% fall which had been generally expected but above July’s revised figure of -0.5%.

“The US LEI declined for a sixth consecutive month, potentially signalling a recession,” said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board.

Short-term US Treasury bond yields jumped on the day, while longer-term yields moved inconsistently. By the close of business, the 2-year Treasury yield had gained 17bps to 4.10%, the 10-year yield had inched up 1bp to 3.54% while the 30-year yield finished 5bps lower at 3.49%.

In terms of US Fed policy, expectations of a higher federal funds range over the next 12 months softened. November contracts implied an effective federal funds rate of 3.74%, 66bps higher than the current spot rate. December contracts implied a rate of 4.06% while September 2023 futures contracts implied an effective federal funds rate of 4.475%, 140bps above the spot rate.

Ozyildirim pointed to a fall in the US manufacturing sector’s average number of work hours per week in four of the last six months as a taste of things to come. “Economic activity will continue slowing more broadly throughout the US economy and is likely to contract. A major driver of this slowdown has been the Federal Reserve’s rapid tightening of monetary policy to counter inflationary pressures.”

Regression analysis suggests the latest reading implies a 1.8% year-on-year growth rate in November, down from October’s figure of 2.3%.