Summary: US Fed’s favoured inflation measure up in March; above market expectations; annual rate accelerates; some signs of “firming inflation pressures”; long-term Treasury bond yields hardly move.

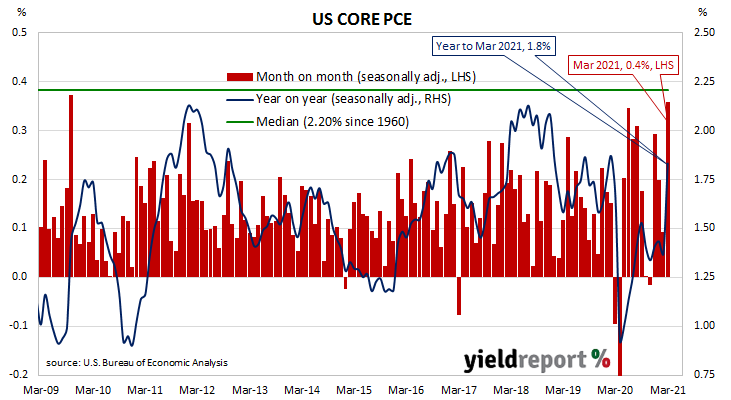

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at the time of 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% before it eased back to a range between 1.5% and 1.8% through 2019. It then plummeted below 1.0% in April 2020 before rising back to around 1.5% in the September quarter.

The latest figures have now been published by the Bureau of Economic Analysis as part of the March personal income and expenditures report. Core PCE prices rose by 0.4% over the month, above the generally expected figure of 0.3% and well above February’s 0.1% increase. On a 12-month basis, the core PCE inflation rate accelerated from 1.4% to 1.8%.

“The PCE deflator showed some evidence of firming inflation pressures in the monthly data as the economy re-opens, but [it is] well within the Fed’s script,” said ANZ Head of Australian Economics David Plank.

US Treasury bond yields hardly moved on the day. By the close of business, the 2-year Treasury bond yield remained unchanged at 0.16%, the 10-year yield had slipped 1bp to 1.53% while the 30-year yield finished unchanged at 2.30%.

The core version of PCE strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used by the Fed; it also tracks the Consumer Price Index (CPI) and the Producer Price Index (PPI) from the Department of Labor. However, it is the one measure that is most often referred to in FOMC minutes.