Summary: Private capital expenditures up 1.1% in September quarter, essentially in line with expectations; up 1.0% on annual basis; Westpac: industries at forefront of underlying structural changes continue investing; ACGB yields down; rate-cut expectations harden; Westpac: industries at coalface of consumer-led slow down pulling back on investment plans,; 2024/25 capex estimate 5.1% higher than previous estimate, 4.3% higher than comparable estimate from 2023/24; Westpac: non-mining sectors facing more pressures to expand capacity to meet demand from rising population, carbon emission targets.

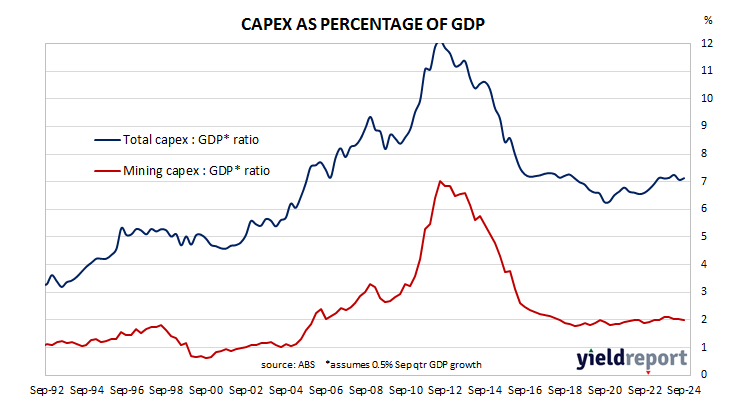

Australia’s private capital expenditure (capex) spiked early in the 2010s on the back of investment in the mining sector. As projects were completed, capex growth rates fell away and generally remained negative for a good part of a decade. Capex as a percentage of GDP is now back to a level more in line with the long-term average.

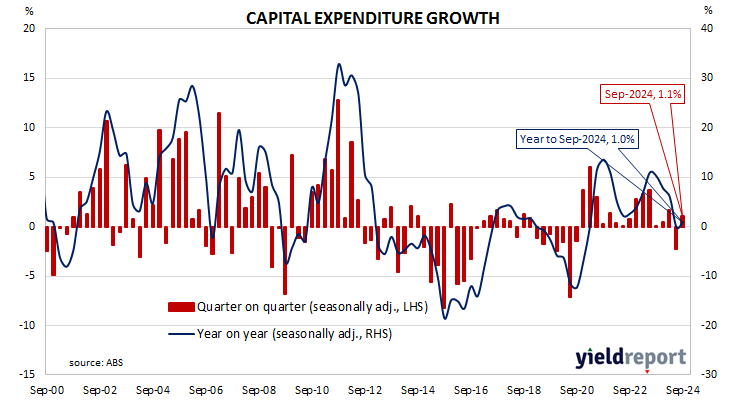

According to the latest ABS figures, seasonally-adjusted private sector capex in the September quarter increased by 1.1%. The result was essentially in line with expectations but in contrast with June quarter’s 2.2% fall. On a year-on-year basis, total capex increased by 1.0%, up from -0.1% in the previous quarter after revisions.

“Today’s outcomes further demonstrates that the industries at the forefront of the underlying structural changes impacting the economy continue to invest and build their capital stocks,” said Westpac senior economist Pat Bustamante. “Electricity generation, information and telecommunications, professional services [and] construction all continue to invest.”

Commonwealth Government bond yields fell almost uniformly across the curve on the day. By the close of business, 3-year and 10-year ACGB yields had both lost 6bps to 3.91% and 4.37% respectively while the 20-year yield finished 5bps lower at 4.71%.

Expectations regarding rate cuts in the next twelve months hardened. Cash futures contracts implied an average of 4.33% in December, 4.295% in February and 4.11% in May. October 2025 contracts implied 3.82%, 52bps less than the current cash rate.

“On the other hand, industries at the coalface of the consumer-led slow down are now clearly pulling back on their investment plans, including wholesale trade, accommodation and food services, retail trade and arts and recreation,” added Bustamante.

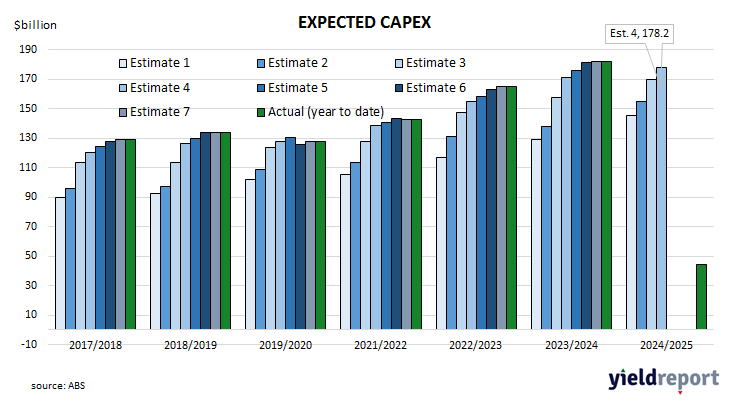

The report also contains capex estimates for the current financial year. The latest capex estimate for the 2024/25 financial year, Estimate 4, is $178.2 billion, 5.1% higher than May’s Estimate 3 and 4.3% higher than Estimate 4 of the 2023/24 financial year.

“Investment in the mining sector has been relatively subdued since the end of the mining boom, while other sectors are facing more pressures to expand capacity and transform their operations to meet the demand of rising population and comply with carbon emission targets,” Bustamante noted. “Indeed, the ABS notes that construction, electricity generation and transport and warehousing revised their expected capex significantly higher over the quarter.”