Summary: US core PCE price index up 0.4% in January, as expected; annual rate slows to 2.8%; ANZ: “super-core” inflation at 3.46% indicates degree of stickiness; Treasury yields fall modestly; Fed rate-cut expectations for 2024 soften a touch; ANZ: some price gains look uncharacteristically strong, expects decline in coming months.

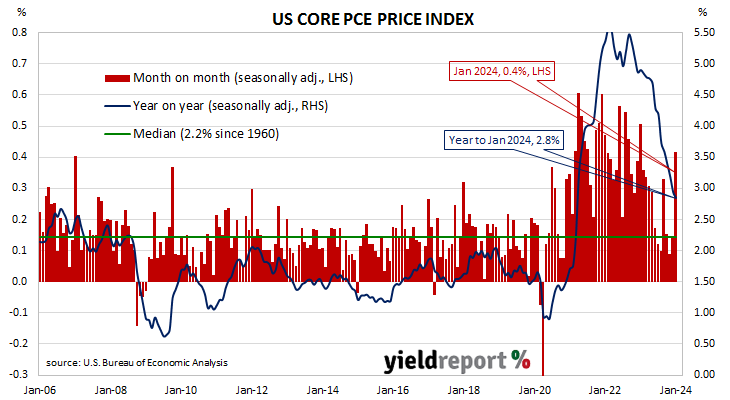

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at the time of 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% before it eased back to a range between 1.5% and 1.8% through 2019. It then plummeted below 1.0% in April 2020 before rising back to around 1.5% in the September quarter of that year. It has since increased significantly and still remains above the Fed’s target even after recent declines.

The latest figures have now been published by the Bureau of Economic Analysis as part of the January personal income and expenditures report. Core PCE prices rose by 0.4% over the month, in line with expectations but up from December’s 0.1% increase. On a 12-month basis, the core PCE inflation rate slowed from December’s rate of 2.9% to 2.8%.

“The super-core measure of PCE inflation, which makes up half of the PCE deflator, rose 0.6%,” said ANZ Head of FX Research Mahjabeen Zaman. “That was its biggest monthly gain since December 2021. The annual rate of super-core inflation was 3.46% versus 3.35% in December, indicating a degree of stickiness.”

US Treasury bond yields fell modestly on the day. By the close of business, 2-year and 10-year Treasury bond yields had both lost 2bps to 4.63% and 4.25% respectively while the 30-year yield finished 3bps lower at 4.37%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened a touch, albeit with several cuts still factored in. At the close of business, contracts implied the effective federal funds rate would average 5.325% in March, essentially in line with the current spot rate, 5.32% in April and 5.195% in June. February 2025 contracts implied 4.375%, 95bps less than the current rate.

“However, some of the price gains within that category looked uncharacteristically strong and we expect they will subside in coming months,” added Zaman. “Prices for financial and insurance services, for example, rose 1.33%.”

The core version of PCE strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It is not the only measure of inflation used by the Fed; the Fed also tracks the Consumer Price Index (CPI) and the Producer Price Index (PPI) from the Department of Labor. However, it is the one measure which is most often referred to in FOMC minutes.