Summary: Euro-zone industrial production up solidly in April; expansion double expected figure; annual growth rate jumps again on “base effects”; supply chain problems still “a drag on growth”; expansion in only two of euro-zone’s four largest economies.

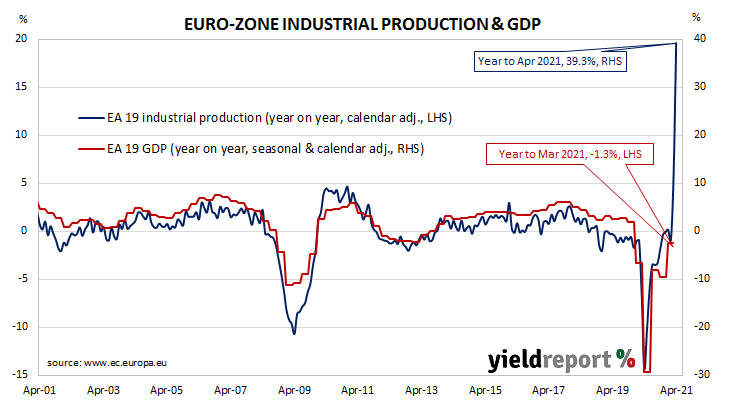

Following a recession in 2009/2010 and the debt-crisis which flowed from it, euro-zone industrial production recovered and then reached a peak four years later in 2016. Growth rates then fluctuated for two years before beginning a steady and persistent slowdown from the start of 2018. That decline was transformed into a plunge in March and April of 2020. However, subsequent months in 2020 and early 2021 produced an almost-complete recovery.

According to the latest figures released by Eurostat, euro-zone industrial production increased by 0.8% in April on a seasonally-adjusted and calendar-adjusted basis. The expansion was double the 0.4% increase which had been generally expected and double March’s 0.4% increase after revisions. On an annual basis, the calendar-adjusted growth rate jumped again, this time from March’s revised rate of 11.5% to 39.3%. (Monthly production figures collapsed during the June quarter of 2020, resulting in significantly lower bases for annual calculations.)

German and French 10-year sovereign bond yields moved higher on the day. By the close of business, both had risen by 3bps to -0.25% and 0.13% respectively.

ANZ economist Charlotte Heck-Parsch pointed to the effects of the June 2020 quarter’s on the annual growth rate and noted supply chain problems “remain a drag on growth.”

Industrial production growth expanded in only two of the euro-zone’s four largest economies. Germany’s production contracted by 0.3% while the comparable figures for France, Italy and Spain were zero, +1.8% and +1.1% respectively.