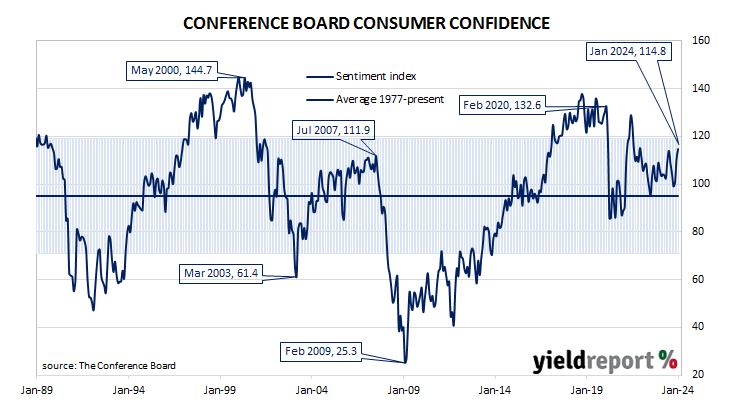

Summary: Conference Board Consumer Confidence Index rises in January, reading more than expected; reflected slower inflation, anticipation of lower interest rates ahead, generally favourable employment conditions; short-term US Treasury yields up, longer-term yields down; expectations of Fed rate cuts in 2024 soften; views of present conditions, short-term outlook improve; gain across all age groups, all incomes groups except very top.

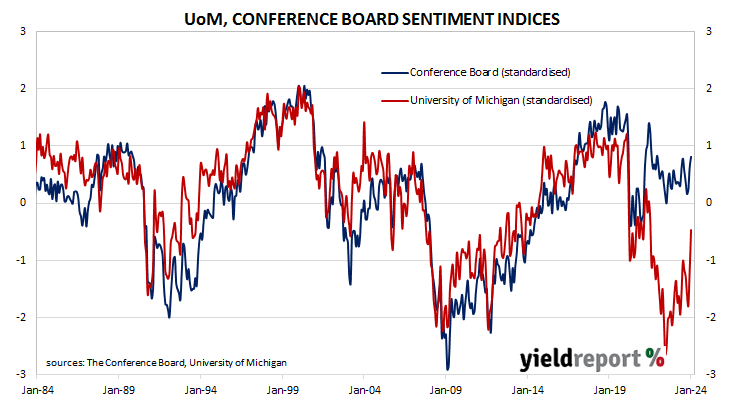

US consumer confidence clawed its way back to neutral over the five years after the GFC in 2008/2009 and then went from strength to strength until late 2018. Measures of consumer confidence then oscillated within a relatively narrow band at historically high levels until they plunged in early 2020. Subsequent readings then fluctuated around the long-term average until March 2021 when they returned to elevated levels. However, a noticeable gap has since emerged between the two most-widely followed surveys.

The latest Conference Board survey held during the first three weeks of January indicated US consumer confidence has improved for a third consecutive month, reversing the deterioration which took place from August through to October. January’s Consumer Confidence Index registered 114.8 on a preliminary basis, above the generally-expected figure of 111.6 as well as December’s final figure of 110.7.

“January’s increase in consumer confidence likely reflected slower inflation, anticipation of lower interest rates ahead, and generally favourable employment conditions as companies continue to hoard labour,” said Dana Peterson, Chief Economist at The Conference Board.

The figures came out at about the same time as the December JOLTS report and short-term US Treasury yields rose while longer-term yields fell. By the close of business, the 2-year Treasury bond yield had gained 5bps to 4.36%, the 10-year yield had lost 2bps to 4.05% while the 30-year yield finished 4bps lower at 4.27%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened, albeit with several cuts still factored in. At the close of business, contracts implied the effective federal funds rate would average 5.325% in February, essentially in line with the current spot rate, 5.29% in March and 5.225% in April. January 2025 contracts implied 4.01%, 132bps less than the current rate.

Consumers’ views of present conditions and their views of the near-future both improved. The Present Situation Index increased from December’s revised figure of 147.2 to 161.3 while the Expectations Index moved up from 81.9 to 83.8.

“The gain was seen across all age groups, but largest for consumers 55 and over. Likewise, confidence improved for all incomes groups except the very top; only households earning $125,000+ saw a slight dip,” Peterson added.

The Consumer Confidence Survey is one of two widely followed monthly US consumer sentiment surveys which produce sentiment indices. The Conference Board’s index is based on perceptions of current business and employment conditions, as well as respondents’ expectations of conditions six months in the future. The other survey, conducted by the University of Michigan, is similar and it is used to produce an Index of Consumer Sentiment. That survey differs in that it does not ask respondents explicitly about their views of the labour market and it also includes some longer-term questions.