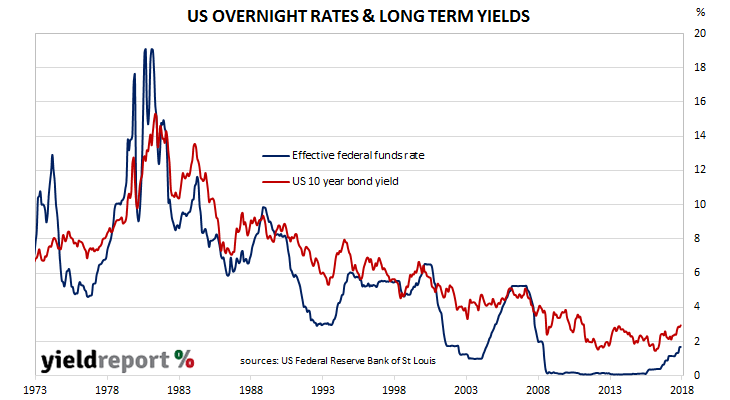

Next month, the Federal Open Market Committee (FOMC) is expected to raise the US Fed’s target range for the federal funds rate by 25bps. Currently, the band sits at 1.50% to 1.75% and the increase will move it to 1.75% to 2.00%. It would be the US central bank’s second increase of the year in which three, possibly four, increases are expected.

The minutes of the FOMC’s latest meeting in early May gave no reason for a change in this view. However, there were one or two sections which gave economists and other observers something to chew on.

The main point of interest was the comment the Fed is happy to let inflation overshoot. ANZ economist Jack Chambers pointed to a section in the minutes discussing this possibility and they “noted that a modest inflation overshoot ‘could be helpful’ ”. He interpreted this statement as a “dovish” sign; that is, even if inflation were to move higher than its 2% target, the statement suggests the FOMC would not necessarily raise the federal funds rate. He also noted the discussion of the yield curve and its predictive powers with regards to recessions. In spite of these points, “the Federal Reserve remains on track to increase rates in June” and once again later in the year. “Overall, the minutes are consistent with a total of three, rather than four, rate hikes this year.”