Summary: Home approval numbers fall; better than expected; home construction still to slow.

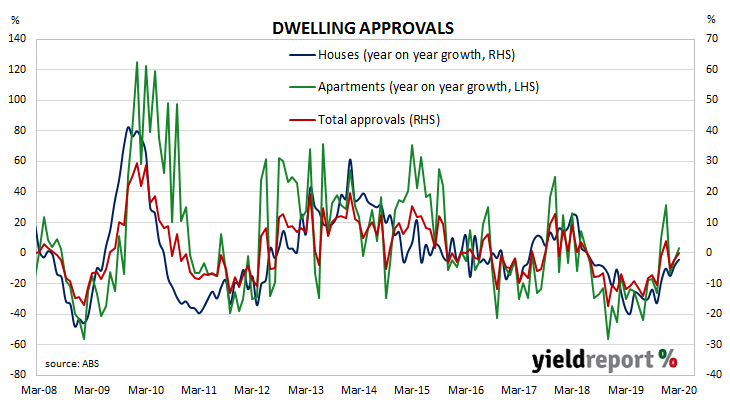

Approvals for dwellings, that is apartments and houses, had been heading south since mid-2018. As an indicator of investor confidence, falling approvals had presented a worrying signal, not just for the building sector but for the overall economy. However, approval figures from late-2019 and early-2020 represented the possibility of a recovery in 2020. Some economists are not convinced.

The Australian Bureau of Statistics has released the latest figures from March and total residential approvals decreased by 4.0% on a seasonally-adjusted basis. The fall over the month was not as bad as the -15% which had been expected but it was still a considerable turnaround from February’s revised figure of +19.4%. Total approvals still increased by 0.2% on an annual basis, an improvement from February’s comparable figure of -4.6% after it was revised up from -5.8%.

ANZ economist Adelaide Timbrell said, “It’s too early to see the impacts of COVID-19 in the building approvals data, since there is a lag between applications and approvals.” Westpac senior economist Matthew Hassan said the fall was “much milder than the expected unwind from a 20% jump the month before.” The figures came out on the same day as the Melbourne Institute’s April Inflation Gauge index and ANZ’s April Job Ads report. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

The figures came out on the same day as the Melbourne Institute’s April Inflation Gauge index and ANZ’s April Job Ads report. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

In the cash futures market, expectations of a rate cut softened a touch. By the end of the day, May contracts implied a rate cut down to zero as a 60% chance, down from the previous day’s 62%. June contracts implied a 56% chance of such a move in that month, down from 58%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 45% and 65%.