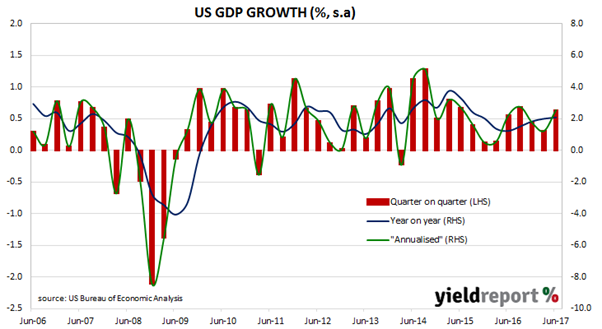

U.S. economics were dominated by two events this week. The first was the FOMC meeting and the second was the release of the June quarter GDP figures. The US Commerce Department released Q2 2017 “advance” estimates of US GDP on Friday night Australian time. This estimate is the first of four estimates and subject to three more revisions over the next two months.

The advance estimates indicate an annualised growth rate of 2.6%, which is broadly in line with the 2.7% median of market estimates but well up on the Q1 2017 figure of 0.7%. Westpac described the difference between the actual and forecast figures as “effectively a rounding error” but a more interesting comment was their observation the figures reinforced the “modest pace” of U.S growth in the first half of 2017. NAB currency strategist Rodrigo Catril saw the good in the figures but at the same time, he acknowledged some roadblocks. “The pace of growth should keep downward pressure on the unemployment rate, but the prospect of higher inflation remains elusive. Meanwhile, amid internal turmoil and Washington paralysis, the prospect of fiscal policy boosting growth above 3% is looking like an almost impossible objective.”