Summary: Non-farm payrolls increase by 678,000 in February; noticeably greater than expected figure; previous two months’ figures revised up by 92,000; jobless rate down to 3.8%, participation rate up; data takes back seat to developments in Ukraine; figures support case rate rise at upcoming FOMC meeting; jobs-to-population ratio increases; underutilisation rate ticks up to 7.2%; annual hourly pay growth slows to 5.1%.

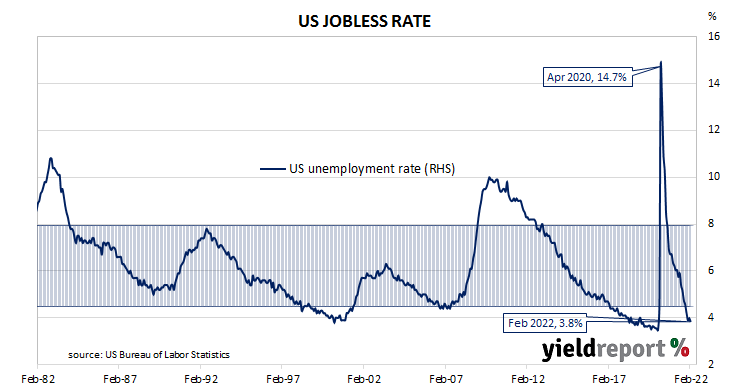

The US economy ceased producing jobs in net terms as infection controls began to be implemented in March 2020. The unemployment rate had been around 3.5% but that changed as job losses began to surge through March and April of 2020. The May 2020 non-farm employment report represented a turning point and subsequent months provided substantial employment gains. Changes in recent months have been generally more modest but usually well above the long-term monthly average.

According to the US Bureau of Labor Statistics, the US economy created an additional 678,000 jobs in the non-farm sector in February. The increase was noticeably greater than the 400,000 which had been generally expected earlier in the week as well as the 481,000 jobs which had been added in January after revisions. Employment figures for December and January were also revised up by a total of 92,000.

The total number of unemployed decreased by 243,000 to 6.270 million while the total number of people who are either employed or looking for work increased by 0.305 million to 163.995 million. These changes led to the US unemployment rate declining from 4.0% in January to 3.8%. The participation rate ticked up from January’s revised rate of 62.2% to 62.3%.

“Whilst US non-farm payrolls came in better than expected, the data took a back seat to the ongoing developments in Ukraine,” said ANZ Head of Australian Economics David Plank.

US Treasury yields fell noticeably on the day as investors moved out of equities and sought low-risk assets. By the close of business, the 2-year yield had lost 4bps to 1.49%, the 10-year yield had shed 11bps to 1.74% while the 30-year yield finished 7bps lower at 2.16%.

In terms of US Fed policy, expectations for a higher federal funds rate over the next 12 months softened noticeably. At the close of business, March contracts implied an effective federal funds rate of 0.205%, 13bps higher than the current spot rate. June contracts implied 0.77% while February 2023 futures contracts implied an effective federal funds rate of 1.66%, 158bps above the spot rate.

Plank noted the figures “support the case” for a 25 basis point rise at the upcoming FOMC meeting “with the possibility of 50 basis point hikes later in the year.”

One figure which is indicative of the “spare capacity” of the US employment market is the employment-to-population ratio. This ratio is simply the number of people in work divided by the total US population. It hit a cyclical-low of 58.2 in October 2010 before slowly recovering to just above 61% in late-2019. February’s reading increased from 59.7% to 59.9%, still some way from the April 2000 peak reading of 64.7%.

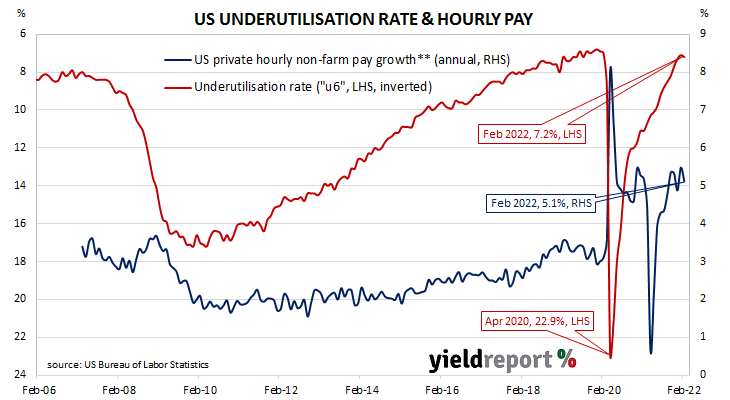

Wage growth spiked in the US during the early stages of pandemic restrictions as lower-paid jobs disappeared at a faster rate relative to higher-paid jobs, disrupting the usual relationship between wage inflation and unemployment rates. Normally, wages tend to grow as the supply of labour tightens.

Apart from the unemployment rate, another measure of tightness in the labour market is the underutilisation rate. The latest reading of it ticked up from January’s 7.1% to 7.2%. Wage inflation and the underutilisation rate usually have an inverse relationship and hourly pay growth in the year to February slowed from January’s revised rate of 5.5% to 5.1%.