Summary: Business conditions deteriorate in July; confidence plummets; shows widespread impacts of lockdowns, NSW drives much of result; “activity conditions will bounce back strongly when restrictions are eased”; capacity utilisation rate declines again; six of eight sectors of economy still at/above respective long-run averages.

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip, declining to below-average levels by the end of 2018. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and the index trended lower, hitting a nadir in April 2020 as pandemic restrictions were introduced. Conditions improved markedly over the next twelve months.

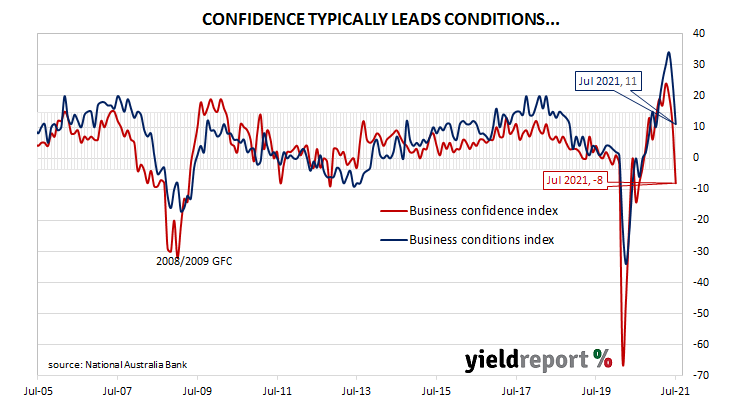

According to NAB’s latest monthly business survey of over 400 firms conducted over the period from 20 July to 30 July, business conditions deteriorated for a second consecutive month. NAB’s conditions index registered 11, down from June’s revised reading of 25.

Business confidence fell for a third consecutive month, to a level below the long-term average. NAB’s confidence index plummeted from June’s reading of 11 to -8. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time. “The survey continues to show widespread impacts of lockdowns,” said NAB senior economist Gareth Spence. “Unsurprisingly, due to its size and the severity of the lockdown in the state, New South Wales drove much of the result this month.”

Commonwealth Government bond yields hardly moved on the day. By the end of it, 3-year and 10-year ACGB yield had each returned to their starting points at 0.33% and 1.20% respectively while the 20-year yield finished 1bp lower at 1.82%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.03%, remained largely unchanged. At the end of the day, contract prices implied the cash rate would creep up to around 0.26% by November 2022.