Summary: May US CPI falls a little more than expected; both headline and core figures just under zero for month; fuel prices, car insurance premiums down; food, rents up; weak inflation “an enduring theme”.

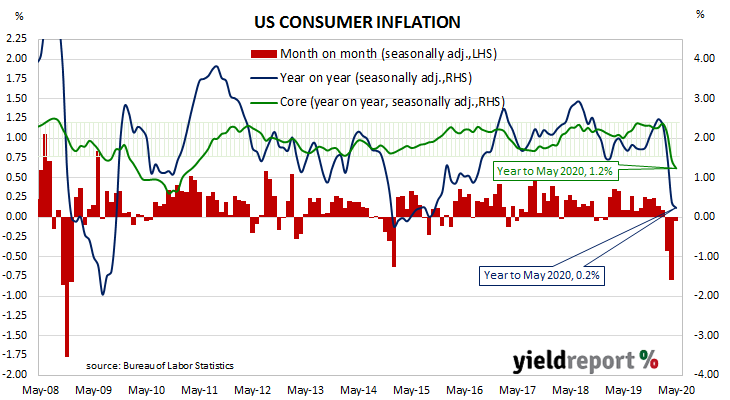

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. “Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. Substantially lower rates for both measures have been reported since March.

The latest CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices decreased by 0.1% on average in May. The fall was just under the flat result which had been expected and a smaller fall than the 0.8% drop recorded in April. On a 12-month basis, the inflation rate slowed from April’s annual rate of 0.4% to 0.2%.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, also decreased on a seasonally-adjusted basis by 0.1% for the month. This too was just under the flat result which had been expected but higher than April’s comparable rate of -0.4%. The annual rate slowed from 1.4% in April to 1.2%, seasonally adjusted.

NAB Head of FX Strategy (FICC division) Ray Attrill said, “The deflationary pulse should ease from here, as activity levels pick up, but a large negative output gap should ensure that weak inflation remains an enduring theme.” ANZ economist Daniel Been was a little harder in his view. “Deflationary risks are clear.”

US Treasury bond yields fell noticeably. The 2-year yield shed 3bps to 0.18%, the 10-year yield lost 11bps to 0.72% and the 30-year yield finished 8bps lower at 1.50%.