Summary: July CPI increase double expected figure; both headline and core figures record large monthly increase; “virus still raging in the US”, “may be some time” before sustained improvement in activity; fuel prices, car insurance premiums up but higher prices of vehicles, clothing and domestic airfare responsible for surprise; Fed unofficial estimate of underlying inflation ticks up.

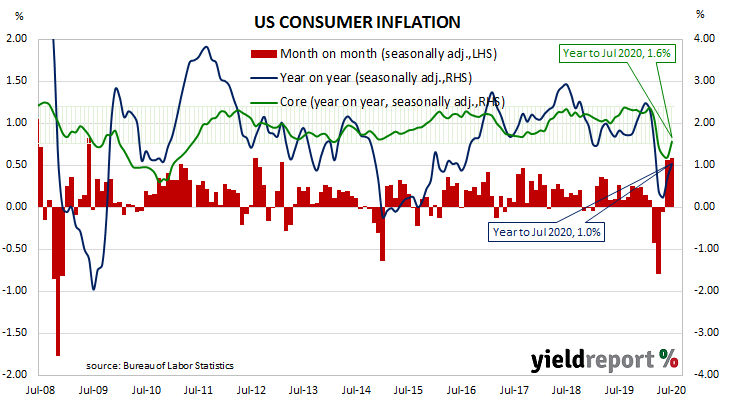

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. “Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. Substantially lower rates for both measures were reported from March to May but recent reports indicate consumer inflation has been rekindled.

The latest CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by 0.6% on average in July. The rise was double the expected figure but the same as June’s increase. On a 12-month basis, the inflation rate accelerated from June’s rate of 0.7% to 1.0%.

“This data and the PPI released a day earlier were both stronger than expected but with the virus still raging in the US it may be some time before there is a sustained improvement in economic activity,” said ANZ FX strategist John Bromhead.

US Treasury bond yields finished higher at the long end. By the end of the day, the US 2-year Treasury yield remained unchanged at 0.15% while 10-year and 30-year yields each finished 3bps higher at 0.67% and 1.36% respectively.

In terms of US Fed policy, expectations of any change in the federal funds range over the next 12 months remained fairly soft. OIS contracts for September implied an effective federal funds rate of 0.072%, or 3.4bps less than the end-of-day spot rate of 0.10%.