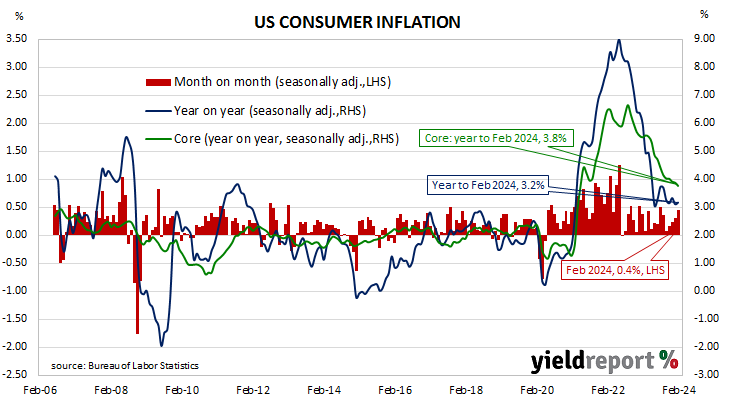

Summary: US CPI up 0.4% in February, in line with expectations; annual inflation rate rises from 3.1% to 3.2%; “core” rate also up 0.4%, up 3.8% over year; Citi: shelter components of CPI likely to remain strong; Treasury yields rise; rate-cut expectations soften; ANZ: 3-month annualised pace is 6.64%, 6-month annualised pace is 5.76; prices of non-energy services main driver again.

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. Substantially lower rates were reported from March 2020 to May 2020 and they remained below 2% until March 2021. Rates then rose significantly before declining from mid-2022.

The latest US CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices rose by 0.4% on average in February. The increase was in line with expectations but up a notch from January’s 0.3% rise. On a 12-month basis, the inflation rate accelerated from 3.1% to 3.2%.

“Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. The core prices index, the index which excludes the more variable food and energy components, also increased by 0.4% on a seasonally-adjusted basis over the month, above consensus expectations of a 0.3% rise. However, the annual growth rate still slowed from 3.9% to 3.8%.

“OER (Owner-Equivalent Rent) moderated to 0.44% after a very strong 0.56% increase in January, helping to reduce the risk of persistently stronger shelter over the next few months,” said Citi economist Veronica Clark. “But we would still caution that shelter components of CPI are likely to remain strong.”

US Treasury bond yields increased on the day. By the close of business, 2-year and 10-year Treasury yields had both gained 6bps to 4.59% and 4.16% respectively while the 30-year yield finished 4bps higher at 4.31%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened, although several cuts are still currently factored in. At the close of business, contracts implied the effective federal funds rate would average 5.33% in March, in line with the current spot rate, 5.325% in April and 5.295% in May. However, September contracts implied a 4.92% rate, 41bps less than the current rate, while February 2025 contracts implied 4.35%, 98bps less than the current rate.

“The 3-month annualised pace is 6.64%, the 6-month annualised pace is 5.76%,” said ANZ economist Kishti Sen. “Given the post-COVID seasonality issues around January-February period, the Fed will look for the data to settle from March.”

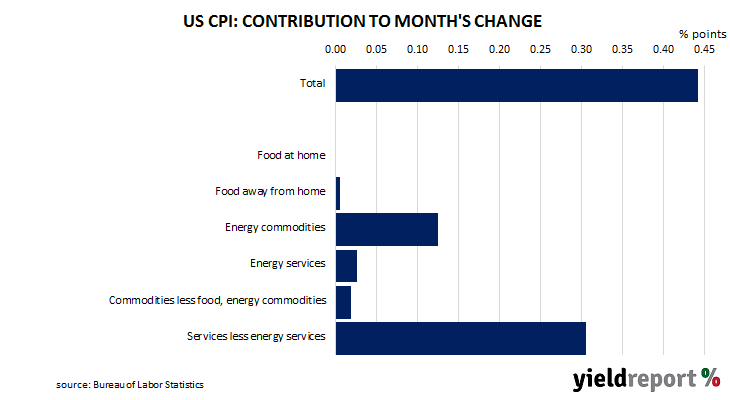

The largest influence on headline results is often the change in fuel prices. Prices of “Energy commodities”, the segment which contains vehicle fuels, increased by 0.8% and contributed 0.12 percentage points to the total. However, prices of non-energy services, the segment which includes actual and implied rents, again had the largest effect on the total, adding 0.30 percentage points after increasing by 0.5% on average.