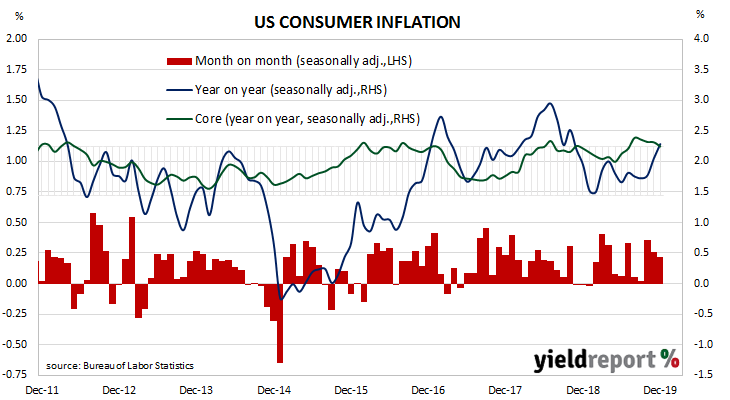

The annual rate of US consumer inflation halved from nearly 3% in the period from July 2018 to February 2019 and then subsequently fluctuated in a range from 1.5% to 2.0%. However, “headline” inflation is known to be volatile and so references are often made to “core” inflation figures for purposes of analysis. This measure has mostly ranged between 1.7% and 2.3% in recent years.

The latest consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.2% in December, in line with the +0.2% increase which had been expected but lower than November’s +0.3%. On a 12-month basis, the inflation rate increased from November’s annual rate of 2.1% to 2.3%. Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.1% for the month, less than the 0.2% which had been expected and less than November’s +0.1% increase. The annual rate slipped from November’s 2.3% to 2.2% in December.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.1% for the month, less than the 0.2% which had been expected and less than November’s +0.1% increase. The annual rate slipped from November’s 2.3% to 2.2% in December.

ANZ senior economist Felicity Emmett said the report “was viewed as a little disappointing, with markets looking for a bit more life in core CPI.”

US Treasury bond yields fell on the day. By the close of trade, the 2-year Treasury yield had lost 3bps to 1.56%, the 10-year yield had fallen by 4bps to 1.81% and the 30-year yield finished 3bps lower at 2.27%.

In the futures market for federal funds, expectations of further rate changes in the short term remained low. According to end-of-day prices of federal funds futures, the implied probability of a 25bps rate cut at either of the FOMC’s January or March meetings remained at zero. July contracts implied a 30% chance of a rate cut, up from the previous day’s 28%.