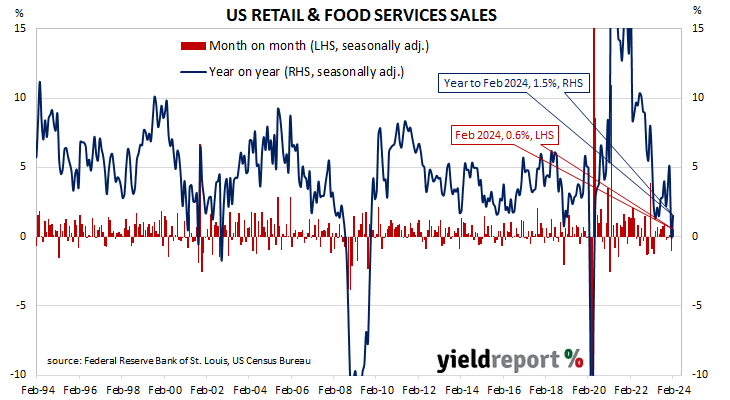

Summary: US retail sales up 0.6% in February, less than expected; annual growth rate accelerates to 1.5%; ANZ: component used to calculate US GDP was flat; US Treasury yields rise; 2024 rate-cut expectations soften; higher sales in nine of thirteen categories; “Motor vehicle & parts dealers” again largest single influence on month’s result.

US retail sales had been trending up since late 2015 but, commencing in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate below 2.0%. Growth rates then increased in trend terms through 2019 and into early 2020 until pandemic restrictions sent them into negative territory. A “v-shaped” recovery then took place which was followed by some short-term spikes as federal stimulus payments hit US households in the first and second quarters of 2021.

According to the latest “advance” numbers released by the US Census Bureau, total retail sales increased by 0.6% in February. The result was less than the 0.8% increase which had been generally expected and in contrast with January’s 1.1% drop after it was revised down from -0.8%. On an annual basis, the growth rate accelerated from January’s revised rate of zero to 1.5%.

“The control group, which strips out food services, auto dealers, building materials stores and gasoline stations and is used to calculate GDP, was flat at 0%, compared to a 0.3% fall in January,” said FX analyst Felix Ryan.

The figures came out at the same time as the latest producer price indices and US Treasury bond yields rose noticeably on the day. By the close of business, the 2-year Treasury yield had added 6bps to 4.69%, the 10-year yield had gained 10bps to 4.29% while the 30-year yield finished 9bps higher at 4.44%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened, although several cuts are still currently factored in. At the close of business, contracts implied the effective federal funds rate would average 5.33% in March, in line with the current spot rate, 5.325% in April and 5.305% in May. However, September contracts implied a 4.975% rate, 36bps less than the current rate, while February 2025 contracts implied 4.44%, 89bps less than the current rate.

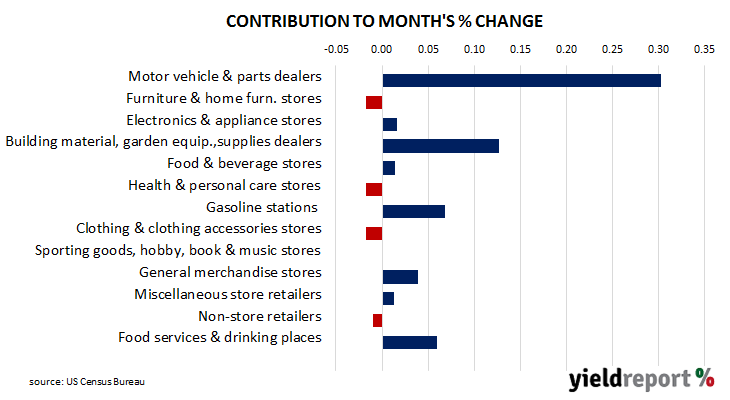

Nine of the thirteen categories recorded higher sales over the month. The “Motor vehicle & parts dealers” segment again provided the largest single influence on the overall result, rising by 1.6% over the month and contributing 0.30 percentage points to the total.

The non-store segment includes vending machine sales, door-to-door sales and mail-order sales but nowadays this segment has become dominated by online sales. It accounts for 17% of all US retail sales and it is the second-largest segment after vehicles and parts.