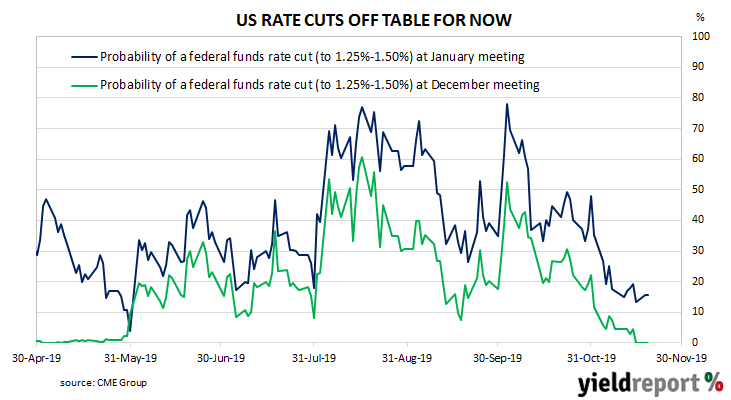

The Fed made its first interest rate increase of this cycle in December 2015. It then raised the federal funds target range another eight times over three years before it began making a series of cuts in what Federal Reserve chief Jerome Powell described as a “mid-cycle adjustment”. The most recent of these three rate cuts was at the FOMC’s meeting at the end of October. The publication of the minutes from that meeting suggests the period of rate cuts may have come to an end. “With regard to monetary policy beyond this meeting, most participants judged that the stance of policy, after a 25 basis point reduction at this meeting, would be well calibrated to support the outlook of moderate growth, a strong labor market, and inflation near the Committee’s symmetric 2 percent objective and likely would remain so as long as incoming information about the economy did not result in a material reassessment of the economic outlook.” In other words, current interest rate settings are appropriate in the absence of data which would change the FOMC’s view.

The publication of the minutes from that meeting suggests the period of rate cuts may have come to an end. “With regard to monetary policy beyond this meeting, most participants judged that the stance of policy, after a 25 basis point reduction at this meeting, would be well calibrated to support the outlook of moderate growth, a strong labor market, and inflation near the Committee’s symmetric 2 percent objective and likely would remain so as long as incoming information about the economy did not result in a material reassessment of the economic outlook.” In other words, current interest rate settings are appropriate in the absence of data which would change the FOMC’s view.

ANZ economist Hayden Dimes said the Fed was concerned about economic conditions despite its apparent intention to keep rates unchanged. “Fed officials still viewed downside risks as elevated but signalled that rates would stay on hold until officials see a ‘material change in their economic outlook.’

US Treasury bond yields finished the day lower. By the end of the day, US 2-year Treasury yields had lost 2bps to 1.57% while 10-year and 30-year yields had each fallen by 4bps to 1.75% and 2.21% respectively.