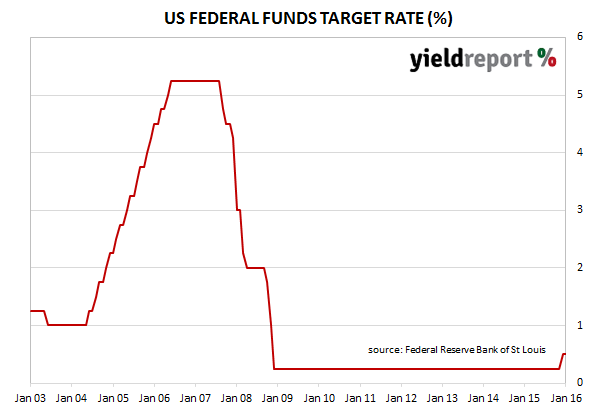

In mid-December, the US Federal Open Markets Committee (FOMC) commenced “lift off”; the first rise in official rates in nearly ten years and the beginning of the latest interest rate cycle. There is, as usual, a lot of conjecture over the pace of interest rate rises with most assuming the trajectory of rate hikes will be much more gradual than in previous rate hike cycles.

At its latest meeting held this week, the FOMC left rates unchanged which was largely as expected. There were no dissenting votes and all voted to maintain the official rate’s target range. The US bond market took the decision in its stride and 2 year bonds barely moved while 10 year bonds edged up 2bps to finish at 0.84% and 2.00% respectively.

Unlike the December meeting there was no post meeting press conference although there was the usual accompanying statement. The statement was similar to September’s as it referred offshore events which were thought to have led to a delay in raising the official rate last year. “The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor (sic) market and inflation, and for the balance of risks to the outlook.”

ANZ said the statement’s cautious tone was to be expected “but the Fed hasn’t deviated from its previous message, with future moves in rates remaining in the hands of the incoming data.”

Westpac noted how the FOMC had downgraded growth and inflation outlooks slightly,

“while appearing to acknowledge the risks which have surfaced since the December meeting. Against that, improvement in the labour market was noted.” Westpac said markets regarded the statement as “dovish”.

Shane Oliver, AMP Capital saw the statement as “dovish” as it acknowledged a strong labour market but referred to slower consumer spending and recent financial market turmoil. He thinks the FOMC will be “backing away from four hikes this year” and one rise or none is more likely.