During the GFC, the U.S. Fed slashed its official rate, known as the federal funds rate, down to zero. It also bought U.S. Treasury bonds and mortgage-backed securities on an unprecedented scale in an attempt to keep yields low while expanding the monetary base*, thus (hopefully) injecting money into the U.S. economy. Eight years later, the U.S. central bank thinks it is time to back away from the emergency measures deemed necessary during and after the GFC.

For some months now, the U.S. Fed has flagged its plan to “normalise” its monetary policy. The first part of its plan involves the raising of the federal funds rate and the first increase occurred in December 2015. The second part involves the disposal of its bond holdings which it plans to do by not reinvesting matured bonds.

For now, markets seem to be sanguine about the gradual removal of such a big holder of bonds from the U.S. market. However, people such as JP Morgan Chase chief Jamie Dimon think the reversal of such a massive programme may have its setbacks. “We’ve never have had QE like this before, we’ve never had unwinding like this before….We act like we know exactly how it’s going to happen and we don’t.”

While there are these sorts of doubts, Westpac’s Rates Strategy team of Damien McColough and Rob Thompson think this part of the normalisation plan will not disrupt financial markets and they make two points as to why they think so.

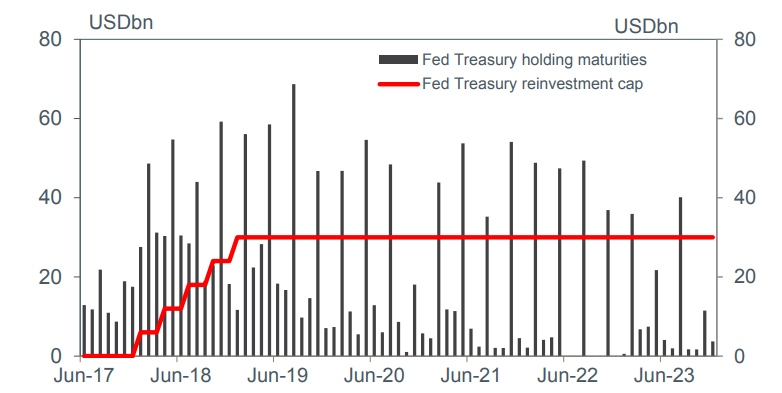

Firstly, the plan will be phased in. Reinvestment will be reduced by USD$6 billion in the first month and USD$12 billion in the second month and so on until reinvestment in any given month is reduced by $30 billion (see below chart). While this may sound like a lot, at one point the U.S. Fed was purchasing USD$80 billion worth of bonds each and every month.

source: Westpac, Federal Reserve