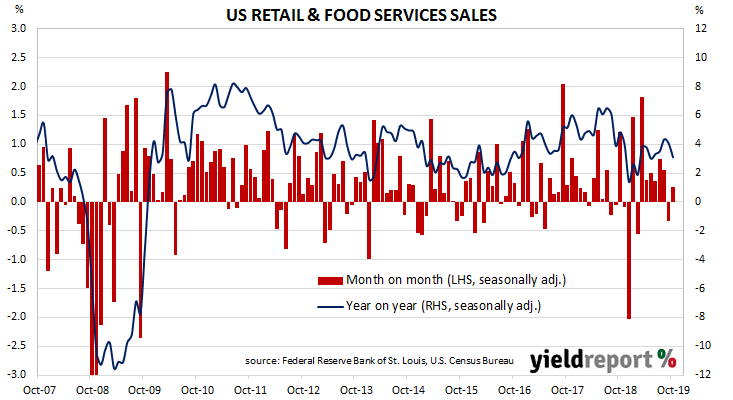

US retail sales had been trending up since late 2015 but, beginning in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of the year. After an unsteady start to 2019, subsequent months’ figures have produced a recovery and expansion which prevailed into the third quarter of the year. However, recent month’s figures have produced some doubts as to the trend’s sustainability.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales grew by 0.3% in October, more than the +0.2% increase which had been expected and a marked turnaround from September’s 0.3% contraction. On an annual basis, the growth rate slowed to 3.1% from September’s rate of 4.1%.

Westpac described the sales figures as “relatively solid and close to estimates.”

Treasury bond yields barely moved on the day, although September’s industrial production figures were released by the Federal Reserve on the same day. By the close of business, the 2-year US Treasury yield remained unchanged at 1.61%, the 10-year rate had crept up 1bp to 1.83% and the 30-year yield remained unchanged at 2.31%.

Treasury bond yields barely moved on the day, although September’s industrial production figures were released by the Federal Reserve on the same day. By the close of business, the 2-year US Treasury yield remained unchanged at 1.61%, the 10-year rate had crept up 1bp to 1.83% and the 30-year yield remained unchanged at 2.31%.

The reaction in the market for federal funds futures was also subdued. The implied probability of a 25bps rate cut at the FOMC’s December meeting fell from 4% to zero while the likelihood of a January cut fell from 19% to 13%.