Summary: US output expands in March; rise less than expected figure; warm weather, supply chain issues blamed; capacity utilisation rate rises, back to December level.

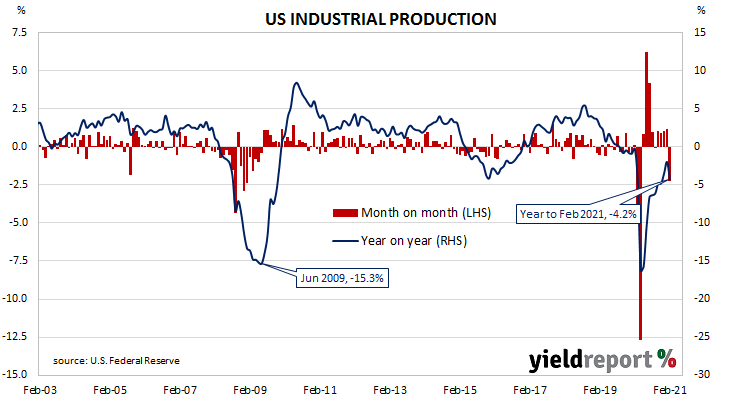

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. US production collapsed through March and April of 2020 and then began recovering in subsequent months.

According to the Federal Reserve, US industrial production grew by 1.4% on a seasonally adjusted basis in March. The result was substantially less than the 3.0% increase which had been generally expected but a marked turnaround from February’s 2.6% contraction after it was revised down from -2.2%. On an annual basis, the expansion rate increased from February’s revised figure of -4.8% to +1.0%.

NAB Head of FX strategy within its FICC division Ray Attrill attributed the failure to fully reverse February’s contraction to “a sharp fall in utility output as the weather dramatically warmed up and auto production impacted by supply shortages” of computer chips.

The report was released on the same day as March’s retail sales numbers and, despite the solid figures, longer-term US Treasury bond yields moved noticeably lower. By the end of the day, the 10-year Treasury yield had lost 5bps to 1.58% and the 30-year yield had shed 4bps to 2.28%. The 2-year yield remained unchanged at 0.15%.