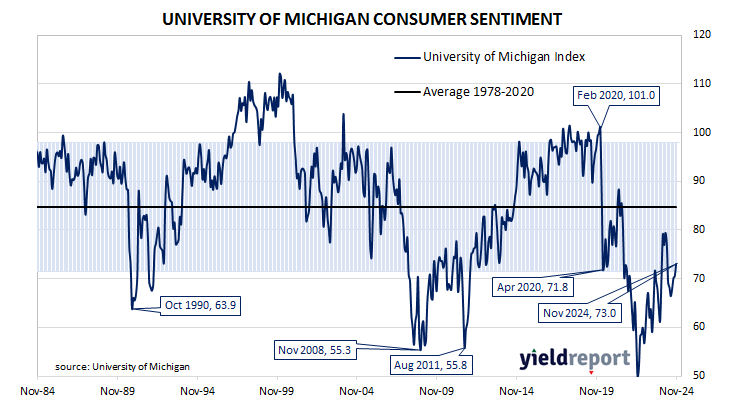

Summary: University of Michigan consumer confidence index rises in November, higher than expected; views of present conditions deteriorate, views of future conditions improve; above June 2022 trough but still below pre-pandemic readings; short-term US Treasury yields rise, longer-term yields fall; rate-cut expectations soften; inflation expectations mixed – short-term down, long-term up.

US consumer confidence started 2020 at an elevated level but, after a few months, surveys began to reflect a growing unease with the global spread of COVID-19 and its reach into the US. Household confidence plunged in April 2020 and then recovered in a haphazard fashion, generally fluctuating at below-average levels according to the University of Michigan. The University’s measure of confidence had recovered back to the long-term average by April 2021 but then it plunged again in the September quarter and remained at historically low levels through 2022 and 2023.

The latest survey conducted by the University indicates confidence among US households has improved somewhat in November. The preliminary reading of the Index of Consumer Sentiment registered 73.0, higher than the 70.6 which had been generally expected and up from October’s final figure of 70.5.

Consumers’ views of current conditions deteriorated while their views of future conditions improved relative to those held at the time of the October survey. The Current Economic Conditions Index slipped from 64.9 to 64.4 while the Index of Consumer Expectations Index increased from 74.1 to 78.5.

“Sentiment is now nearly 50% above its June 2022 trough but remains below pre-pandemic readings,” said the University’s Surveys of Consumers Director Joanne Hsu. “Note that interviews for this release concluded on Monday and thus do not capture any reactions to election results.”

Short-term US Treasury bond yields rose moderately on the day while longer-term yields fell. By the close of business, the 2-year Treasury yield had gained 5bps to 4.16%, the 10-year yield had lost 2bps to 4.31% while the 30-year yield finished 7bps lower at 4.47%.

In terms of US Fed policy, expectations of a lower federal funds rate in the next 12 months softened, although another three 25bp cuts are still priced in. At the close of business, contracts implied the effective federal funds rate would average 4.505% in December, 4.405% in January and 4.315% in February. October 2025 contracts implied 3.84%, 74bps less than the current rate.

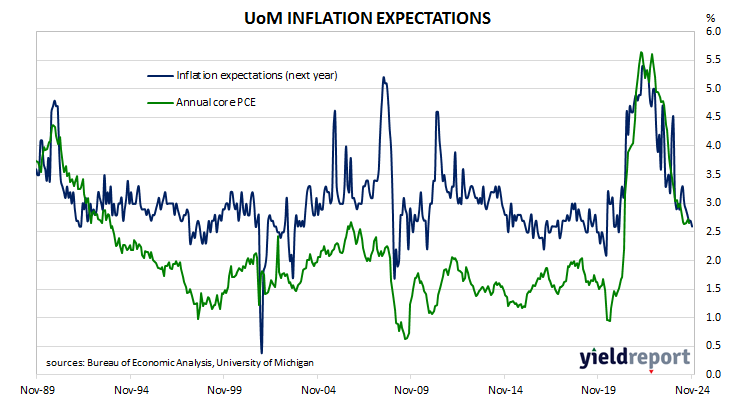

US consumer inflation expectations eased in the short-term while longer-term expectations increased slightly. Year-ahead expectations slowed from 2.7% to 2.6% but long-term expectations ticked up from 3.0% to 3.1%.

It was once thought less-confident households are generally inclined to spend less and save more; some decline in household spending could be expected to follow. However, recent research suggests the correlation between household confidence and retail spending is quite weak.