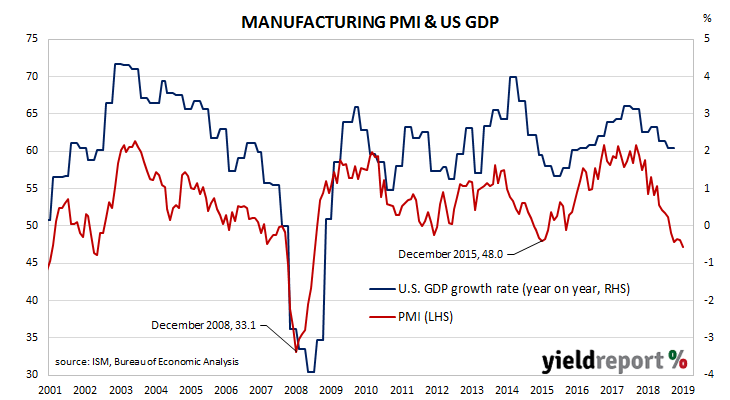

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Recent months’ readings appear to have stabilised, albeit at sub-neutral levels.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 47.2 for December, down from November’s reading of 48.1 and less than the market’s expected figure of 49. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

Despite the lower reading, the ISM’s Tim Fiore said “there are signs that several industry sectors will improve as a result of the phase-one trade agreement between the U.S. and China.”

Westpac’s economics team noted the ISM’s positive response to the figures. “Although the profile is one of contraction in production, the ISM write up suggested that sentiment was actually improving vs Q3 [the September quarter] and, despite global concerns, the report cited improvements due to the phase one trade deal with China.”

US Treasury yields fell noticeably across the curve but the falls were more a function of safe haven purchases prompted by news of the US assassination of a senior Iranian general. By the end of the day, the 2-year Treasury bond yield had lost 4bps to 1.53%, the 10-year yield had fallen by 9bps to 1.79% while the 30-year yield finished 8bps lower at 2.25%.

US Treasury yields fell noticeably across the curve but the falls were more a function of safe haven purchases prompted by news of the US assassination of a senior Iranian general. By the end of the day, the 2-year Treasury bond yield had lost 4bps to 1.53%, the 10-year yield had fallen by 9bps to 1.79% while the 30-year yield finished 8bps lower at 2.25%.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of a rate cut remained slim. The implied likelihood of a 25bps cut at the January meeting of the FOMC remained at zero while a move in March increased from 4% to 8%.