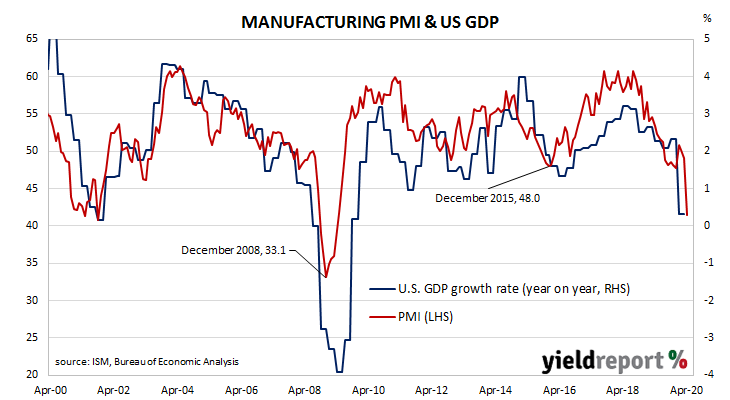

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Readings stabilised in late 2019 after a truce of sorts was made with the Chinese regarding trade. However, the March 2020 report implied US manufacturing activity had begun contracting and the latest reading has all but confirmed it.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 41.5 in April, higher than the expected figure of 37.5 but much, much lower than March’s final reading of 49.1. The average reading since 1948 is 52.8 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “The coronavirus pandemic and global energy market weakness continue to impact all manufacturing sectors for the second straight month. Among the six big industry sectors, Food, Beverage and Tobacco Products remains the strongest. Transportation Equipment and Fabricated Metal Products are the weakest of the big six sectors.” US Treasury yields fell at the long end of the curve. By the end of the day, the 2-year Treasury bond yield had crept up 1bp to 0.20% while the 10-year yield had gained 2bps to 0.62% and the 30-year yield finished 4bps higher at 1.25%.

US Treasury yields fell at the long end of the curve. By the end of the day, the 2-year Treasury bond yield had crept up 1bp to 0.20% while the 10-year yield had gained 2bps to 0.62% and the 30-year yield finished 4bps higher at 1.25%.

NAB head of FX Strategy within its FICC division Ray Attrill said the index had been “once again held up by the rise in supplier delivery times, a function of the lockdowns and disrupted supply chains [and] not excess demand…” He also noted a fall of the new orders sub-index below the GFC-era record low, as well as falls in other sub-indices to record or near-record lows.