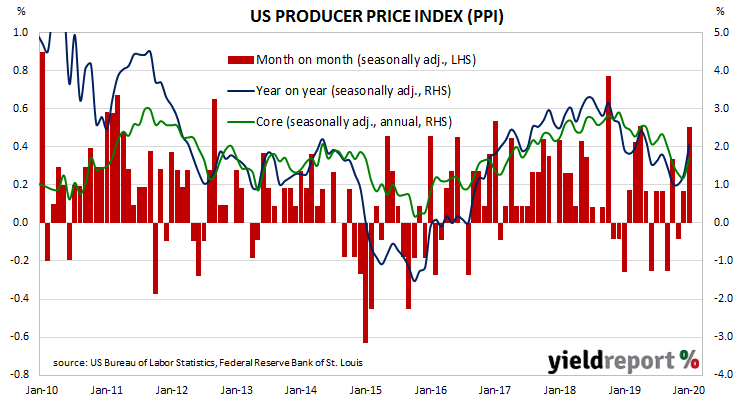

Around the end of 2018, the annual rate of prices received by producers began a downtrend which then continued through 2019. Months in which prices picked up suggested the trend may have been coming to an end, only for the trend to continue. It is tempting to suggest the most recent figures represent a change.

The figures from January have been published by the Bureau of Labor Statistics and they indicate producer prices increased by 0.5% after seasonal adjustments, more than the 0.1% which had been expected and an increase from December’s revised increase of 0.2%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments accelerated to 2.1% after recording 1.3% in December and 1.0% in October.

ANZ economist Kishti Sen Hayden Dimes said the result was much stronger than expected but “largely due to a 0.7% rise in services costs, as strong rises in retailer margins offset weakness in freight and cargo.” However, he described inflationary pressures overall as “subdued”.

“Core” PPI inflation also increased by 0.5%, a marked increase from December’s 0.1% rise. Its annual rate accelerated to 1.7% from 1.2% after having slowed for four consecutive months.

US Treasury bond yields finished higher but only at the short end. By the end of the day, the US 2-year Treasury yield had increased by 2bps to 1.42% while 10-year and 30-year yields each remained unchanged at 1.56% and 2.01% respectively.