Summary: US producer price index (PPI) up 1.1% in June, greater than expected; annual rate rises to 11.2%; “core” PPI up 0.4%; fuel prices again a big driver; US Treasury yields, rate-rise expectations, move haphazardly; business margins show firms still retain strong pricing power.

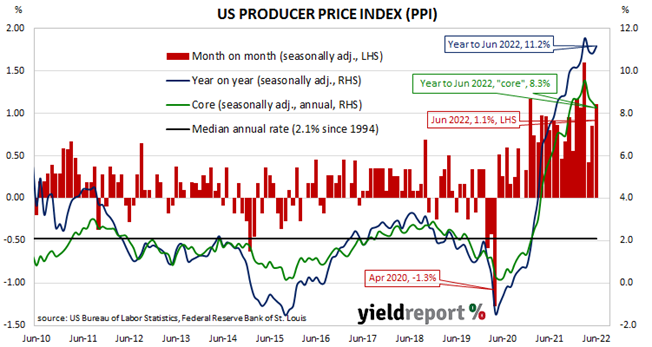

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which continued through 2019. Months in which producer prices increased suggested the trend may have been coming to an end, only for it to continue, culminating in a plunge in April 2020. Figures returned to “normal” towards the end of that year but annual rates over the past eighteen months have been well above the long-term average.

The latest figures published by the Bureau of Labor Statistics indicate producer prices rose by 1.1% after seasonal adjustments in June. The increase was greater than the 0.8% which had been generally expected as well as May’s revised increase of 0.9%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments accelerated from May’s revised rate of 10.8% to 11.2%.

Producer prices excluding foods and energy, or “core” PPI, rose by 0.4% after seasonal adjustments. The increase was less than the 0.5% rise which had been generally expected as well as May’s 0.6% after it was revised up from 0.5%. The annual rate slowed from May’s revised figure of 8.5% to 8.3%.

“High fuel prices again a big driver in the June number and the numbers paint a too-high inflation picture to be sure, but in contrast to the CPI a day earlier the detail didn’t make for as universally gloomy reading,” said NAB economist Taylor Nugent.

US Treasury bond yields moved haphazardly on the day. By the close of business, the 2-year Treasury yield had slipped 1bp to 3.14%, the 10-year yield had gained 3bps to 2.96% while the 30-year yield finished 1bp lower at 3.11%.

In terms of US Fed policy, expectations of higher federal funds rates through to March 2023 softened somewhat while simultaneously hardening for months further out. At the close of business, July contracts implied an effective federal funds rate of 1.69%, 11bps higher than the current spot rate. September contracts implied 2.625% while July 2023 futures contracts implied an effective federal funds rate of 3.365%, nearly 180bps above the spot rate.

ANZ economist Kishti Sen said recent months’ increases in business margins show “firms still retain strong pricing power”, thus implying “core CPI inflation will remain high in coming months, especially as service prices are generally sticky.”

The producer price index is a measure of prices received by producers for domestically produced goods, services and construction. It is put together in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective rather than from the perspective of a retailer or a consumer. It is another one of the various measures of inflation tracked by the US Fed, along with core personal consumption expenditure (PCE) price data.