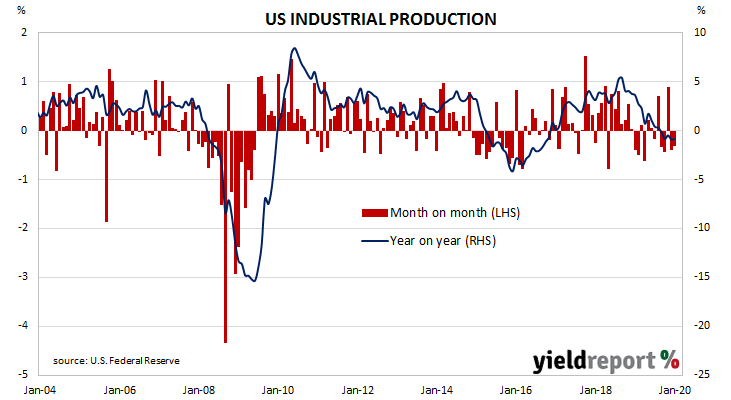

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. The latest figures indicate a downtrend which began in late 2018 has continued.

According to January’s figures released by the Federal Reserve, US industrial production fell by 0.3%, in line with expectations and a little higher than December’s revised figure of +0.4%. On an annual basis, the growth rate improved from December’s -0.9% to -0.8%. The report came on the same day as consumer sentiment and retail sales figures were released and bond yields fell a few basis points across the curve. By the close of trade, the 2-year Treasury yield was 2bps lower at 1.42% while 10-year and 30-year yields had both lost 3bps each to 1.59% and 2.04% respectively.

The report came on the same day as consumer sentiment and retail sales figures were released and bond yields fell a few basis points across the curve. By the close of trade, the 2-year Treasury yield was 2bps lower at 1.42% while 10-year and 30-year yields had both lost 3bps each to 1.59% and 2.04% respectively.

In terms of US Fed policy, expectations of another rate change in the next few months remained soft. According to end-of-day prices of federal funds futures, the implied probability of a 25bps rate cut at the FOMC’s March meeting ticked up from 10% to 11%, while the likelihood of a rate cut by or at July’s meeting moved from 55% to 56%.