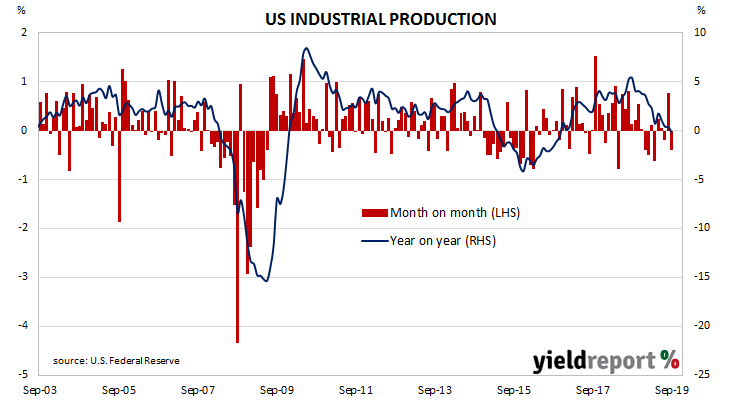

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. A month ago, IP figures had suggested some chance of an end to a recent run of months in which US production has gone backwards. Figures from the latest report indicated that view was probably premature.

According to the latest figures released by the Fed, US industrial production slumped by 0.4% in September, less than the 0.2% fall which had been expected and a noticeable turnaround from August’s revised growth rate of +0.6%. On an annual basis, growth in industrial production slowed from August’s revised rate of +0.4% to -0.1%.

Westpac’s Finance AM team said the figures “appeared softer but much of that was due to upward revisions to the prior month.” Over at NAB, currency strategist Rodrigo Catril was less forgiving. “Industrial production was weak, not helped by the GM strike but even excluding that the manufacturing sector looks fragile.”

Treasury bond yields finished the day a touch higher, moving the yield curve consistently up. By the close of business, 2-year, 10-year and 30-year US Treasury yields had all inched up 1bp to 1.59%, 1.75% and 2.24% respectively.