Sometime good news is viewed by financial markets as bad. In other times, the same news can be taken as good. In this case, while the news in question has not been viewed as good, what was generally seen as bad on the surface had been interpreted as being alright, if not slightly favourable.

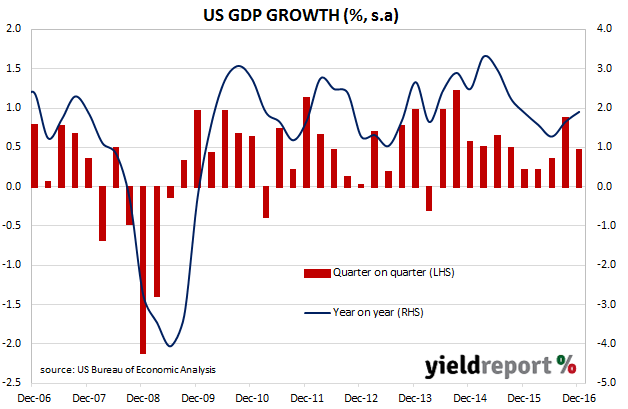

The US Commerce Department released Q4 “advanced” estimates of US GDP on Friday night Australian time. This estimate is the first of four estimates and subject to three more revisions over the next two months. They show an annualised growth rate of 1.9%, lower than the median estimate of 2.1% and well down up on the Q3 2016 figure of 2.9%.

Yields of US Treasury bonds did not alter much after the report. 2 year bond yields were essentially unchanged on the day at 1.22% and 10 year bonds were 2bps lower at 2.48%. The rationale for this is in the composition of GDP. Net exports were the main culprit because imports were higher. Strong economies suck in imports and so in a counter-intuitive manner, a higher net export figure which leads to a smaller GDP figure is indicative of strong domestic demand.

ANZ said the numbers “disappointed” but the bank pointed to “firm” private consumption figures as well other data it described as ”encouraging”. Westpac’s view was similar but it too found something positive in the figures when it said “the underlying detail was decent and inflation expectations ticked higher.”

US GDP numbers are published in a manner which is different to most other countries; quarterly figures are compounded to give an annualised figure. In countries such as Australia and the UK, an annual figure is calculated by taking the latest number and comparing it with a figure from a year ago. The diagram below shows US GDP once it has been expressed in the normal manner.