Summary: retail sales stage large bounce in May; however, still negative on annual basis; all segments make gains; June quarter GDP forecasts may be revised.

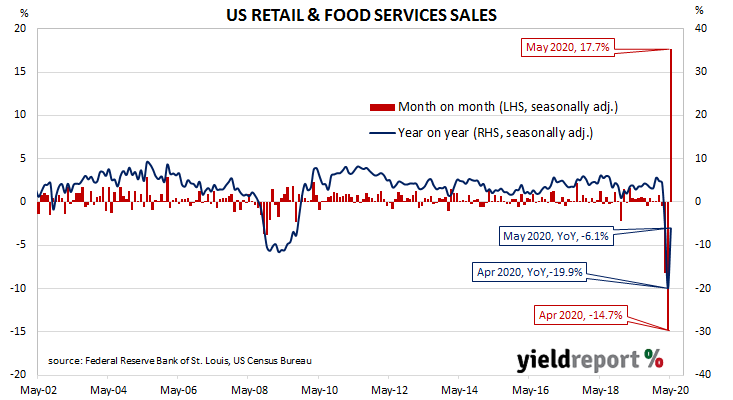

US retail sales had been trending up since late 2015 but, commencing in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of that year. Growth rates then increased in trend terms through 2019 and into early 2020, until restrictions on American households began to take effect in March.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales leaped by 17.7% in May. The gain was a much greater one than the 7.4% which had been expected and it was an incredible turnaround from April’s revised figure of -14.7%. On an annual basis, the growth rate recovered to -6.1% from April’s revised rate of -19.9%.

The report came out on the same day as May’s industrial production and capacity utilisation report. US Treasury bond yields finished higher, especially at the ultra-long end. By the end of the day, the US 2-year Treasury yield remained unchanged at 0.20% while the 10-year yield had gained 2bps to 0.75% and the 30-year yield had jumped 9bps higher to 1.55%

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months retained an easing bias. OIS contracts from July onwards continued to imply some chance of a move to a zero effective federal funds rate.

“The bounce in retail sales is remarkable and confirms the narrative seen in high-frequency data of activity having troughed in mid-April and recovering ever since,” said NAB economist Tapas Strickland. He also said the figures implied US June quarter GDP “may not be as weak as first thought given the strong bounce in May and a likely repeat in June…” and “advanced economies consumption might recover faster than the industrial side due to government payments offsetting lost income…”