Central banks around the world want higher inflation and they are doing their best to create it with a suite of measures. Ultra-low interest rates and injections of new cash in exchange for bonds have been used to stimulate investment and consumer spending in the economies of the US, Europe, the UK and Japan. Whether these policies have been or will be successful is a matter for debate but so far, only the US has halted additional bond purchases and only after USD$3.7 trillion was injected into its economy over the past eight years.

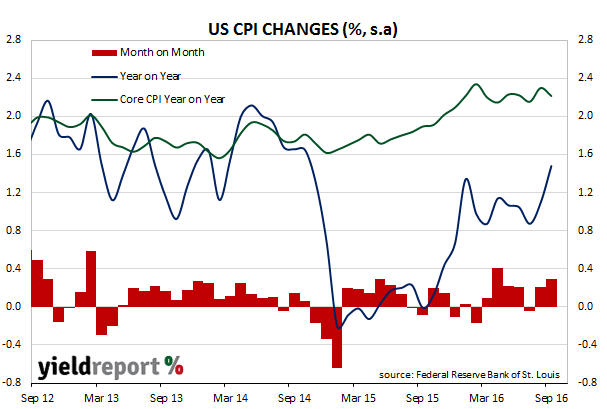

Monthly inflation figures are the scoreboard, so to speak, measuring whether central banks are winning or not and in the US, the game is still in progress. September CPI figures released by the Bureau of Labor Statistics indicate consumer prices rose 0.3% for the month, 1.5% for the year and in line with market forecasts. Core prices, the measure of prices which strips out food and energy prices changes, rose 0.1% for the month, which is less than expected. Over the last 12 months, core inflation slipped from August’s 2.3% to 2.2% (seasonally adjusted).

According to the Bureau, the rise in the overall price level was driven by housing costs and fuel prices, with fuel accounting for half of the overall rise. In the core CPI measure, prescription drug prices had the largest increase at 0.8% for the month. ANZ Research viewed the figures as “good news for the FOMC achieving its dual mandate” but Westpac was less positive and said the figures were “slightly disappointing” as the core measure of CPI was lower than the previous month.

US yields initially rose on the news but finished the day lower. The US 2 year yield fell 2bps to 0.80% and 10 year yield finished 3bps lower at 1.74%. The USD was slightly higher against other currencies, which is the currency markets’ way of implying a higher probability on US rate rises but cash markets contract implied a slightly lower probability of a rate rise at December’s FOMC meeting.