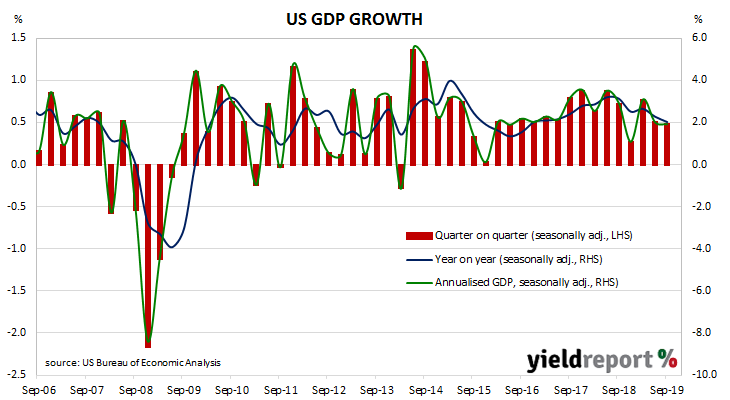

While the US has a historically low unemployment rate, bond yields suggest future growth rates will be below trend. The US Fed has been cutting rates as a form of insurance against a softening external sector and the yield curve is close to being flat after having been inverted for a short period according to at least two measures. While US GDP growth figures have softened through the first half of calendar 2019, they have been far from recessionary.

The US Commerce Department has now released September quarter “advance” GDP estimates and they indicate the US economy grew at an annualised growth rate of 1.9%. The growth figure was more than the 1.6% expected but it represents a minor reduction from the June quarter’s revised figure of 2.0%.

NAB senior economist David de Garis described the increase as a surprise which had come about as a result of “slightly stronger consumption growth”. Overall, the figures were “consistent with the moderation in a broad range of US economic indicators this year.”

The report came out on the same day as the ADP’s employment report and on the same day the FOMC cut the federal funds target range by 25bps. US Treasury bond yields moved lower, especially at the long end. By the end of the day, 2-year Treasury bond yields were 4bps lower at 1.60% while 10-year and 30-year yields had each lost 7bps to 1.77% and 2.26% respectively.