Summary: Private sector credit barely grows in September; “weakest for private sector credit since GFC”; steady growth in owner-occupier segment again offset by falls in business loans, personal debt.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but they disappeared in April.

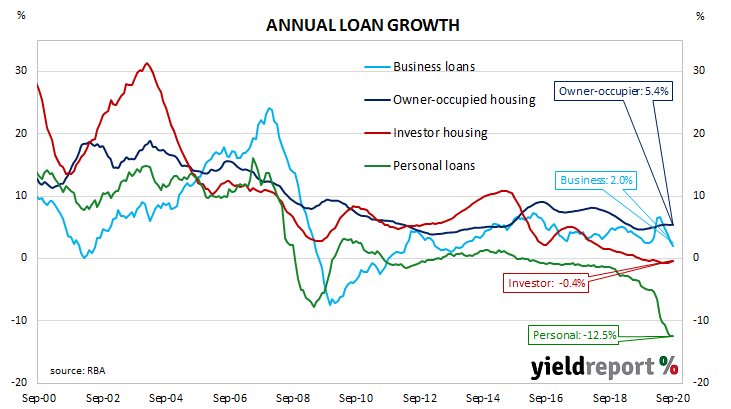

According to the latest RBA figures, private sector credit grew by 0.1% in September, the first increase since March. The result was in line with expectations and above August’s flat result. However, the annual growth rate slowed to 2.0% from August’s comparable rate of 2.2%.

“These results are the weakest for private sector credit since the GFC. In that cycle, annual growth slowed to a low of 0.8% in November 2009, including a 7.5% decline for business. The low in the early 1990s recession period was -1.8% in April 1992,” said Westpac senior economist Andrew Hanlan.

Owner-occupier loans continued to grow steadily but their growth was again largely offset by falls in business loans and personal debt.

Long-term Commonwealth bond yields moved a little higher. By the end of the day, the 10-year ACGB yield had inched up 1bp to 0.83% and the 20-year yield had gained 2bps to 1.44%. The 3-year yield finished unchanged at 0.17%.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.5% over the month, up from August’s 0.4%. The sector’s 12-month growth rate remained at 5.4%.

Growth rates in the business sector resumed their downtrend in May and it has continued through to September as business credit contracted by 0.3%, a slightly slower rate of contraction than the 0.4% fall in August. The segment’s annual growth rate slowed from August’s rate of 2.9% to 2.0%.