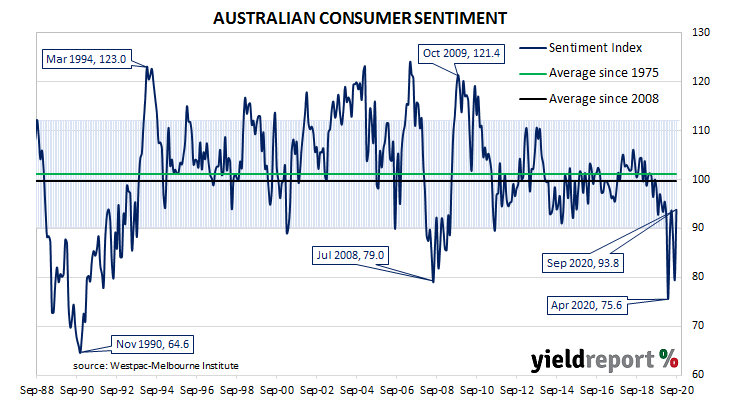

Summary: Household sentiment bounces significantly, continuing recent erratic path; confidence index back to pre-pandemic level; weakness in other states due to virus clusters and possible “second wave”; survey carried out prior to Victorian announcement of slow reopening; Vic disappointment may be offset by containment success.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April and then went through a series of partial recoveries which were followed by bouts of pessimism.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of September, household sentiment has bounced back, continuing an erratic path. The Consumer Sentiment Index jumped from 79.5 to 93.8, taking it back to the levels recorded prior to the introduction of pandemic restrictions.

“We suspected last month’s 9.5% collapse in the Index was an over-reaction but this month’s 18% rebound is a pleasant surprise nonetheless,” said Westpac chief economist Bill Evans. “The rebound means the Index is now just 1.6% below the average over the six months prior to the emergence of COVID-19 in March.”

Local Treasury bond yields fell, especially at the long end, largely following US Treasury movements in overnight trading. By the end of the day, the 3-year ACGB yield had shed 2bps to 0.29%, the 10-year yield had lost 7bps to 0.91% while the 20-year yield finished 8bps lower at 1.49%.

In the cash futures market, expectations of a change in the actual cash rate remained fairly stable. By the end of the day, contracts implied the cash rate would remain in a range of 0.11% to 0.12% through to the latter part of 2021.

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure has returned to the low end of the normal range, below the long-term average reading of just over 101.