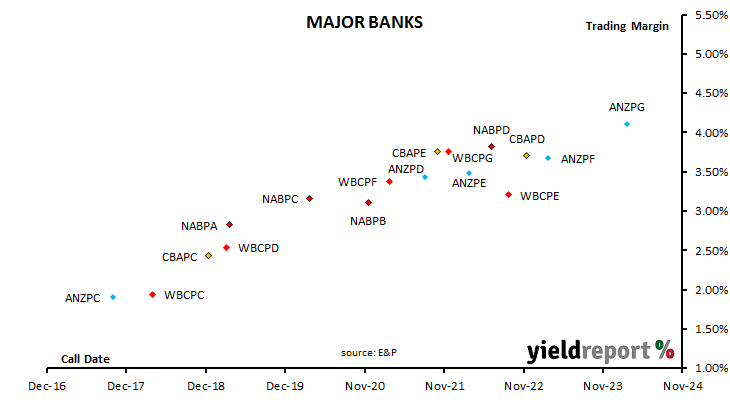

Evans & Partners’ Head of Income Products, Michael Saba thinks Westpac’s Capital Notes 2 (ASX code: WBCPE) stands out and not for the right reasons. “The scatter plot shows WBCPE to be still too low in margin with better value in shorter dated issues. ANZPG tends to top the volume list most days however it sits about right given its longer maturity profile.”

Its annual coupon, is equal to 90 day BBSW + 305bps (inclusive of franking credits). Sometimes investors focus on the income part of a hybrids return but given its coupon is not particularly high relative to other existing hybrids issued by major banks, this does not appear to be the motivation behind investor demand. Perhaps it is just another price anomaly which has built up over time.

As at close of business 17/01/2017