Summary: Leading index growth rate falls again in July; “still consistent with above-trend growth”; reading implies annual GDP growth to rise to around 4.0% during third, fourth quarters; Westpac slashes September quarter growth forecast from -0.7% to -2.6%; expects bounce in December quarter.

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings were markedly higher but more-recent readings have steadily declined.

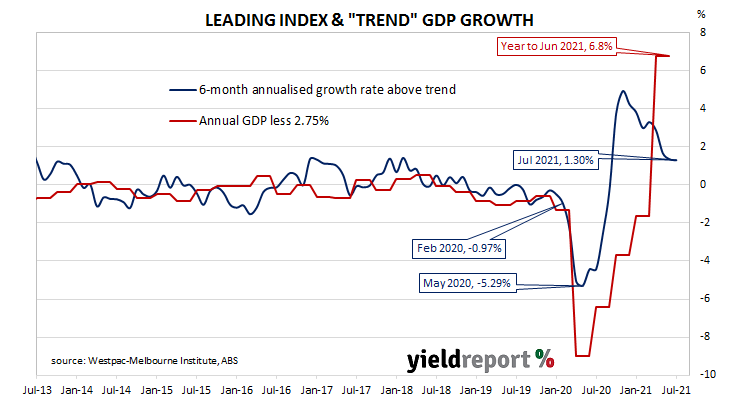

The latest reading of the six month annualised growth rate of the indicator fell in July, from June’s revised figure of +1.36% to +1.30%.

“The Leading Index continues to slow but is still consistent with above-trend growth over the next three to nine months,” said Westpac Chief Economist Bill Evans.

Index figures represent rates relative to “trend” GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by up to nine months, so theoretically the current reading represents an annual GDP growth rate of around 4.0% in the third or fourth quarters of 2021.

Domestic Treasury bond yields moved lower on the day. By the close of business, 3-year and 10-year ACGB yields had each shed 2bps to 0.24% and 1.11% respectively while the 20-year yield finished 3bps lower at 1.75%.

A month ago, Westpac slashed its September quarter GDP growth forecast from 0.9% to -0.7%. Evans cut this forecast again, this time to -2.6% given “the deteriorating outlook in New South Wales and Melbourne.” However, he currently expects a 2.6% increase in the December quarter and “very strong growth” in 2022.