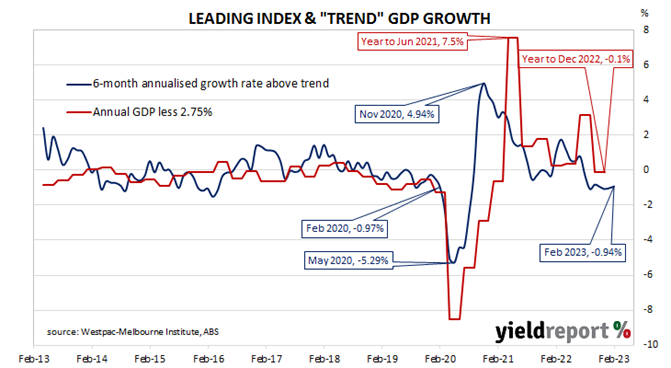

Summary: Leading index growth rate up in February; seventh consecutive month of below-trend results; reading implies annual GDP growth of around 1.75%; ACGB yields higher; rate-rise expectations firm; offshore banking problems have indirect implications for domestic growth.

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings spiked towards the end of 2020 but then trended lower through 2021, 2022 and now 2023.

The February reading of the six month annualised growth rate of the indicator registered -0.94%, up a little from January’s figure of -1.04%.

Westpac Chief Economist Bill Evans noted the latest figures represent the seventh consecutive month in which the index’s six-month growth rate has been negative.

Index figures represent rates relative to “trend” GDP growth, which is generally thought to be around 2.75% per annum in Australia. The index is said to lead GDP by “three to nine months into the future” but the highest correlation between the index and actual GDP figures occurs with a three-month lead. The current reading thus represents an annual GDP growth rate of around 1.75% in the next quarter.

Domestic Treasury bond yields increased substantially, outpacing the large rises of US Treasury yields overnight. By the close of business, 3-year and 19-year ACGB yields had both gained 18bps to 2.96% and 3.37% respectively while the 20-year yield finished 13bps higher at 3.80%.

In the cash futures market, expectations regarding future rate rises firmed, somewhat reversing the previous day’s movements. At the end of the day, contracts implied the cash rate would remain essentially steady at the current rate of 3.57% to average 3.575% in April and 3.61% in May. August contracts implied a 3.505% average cash while November contracts implied 3.40%.

Evans does not expect any significant impact on Australia’s financial system from the various bank collapses in Europe and the US. However, he does expect tightening financial conditions in these regions to “have indirect implications for Australia’s growth prospects.”