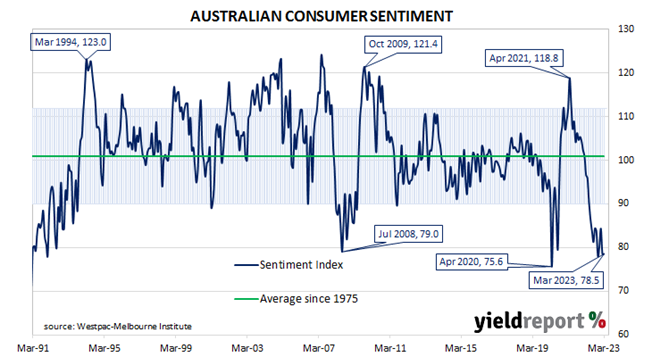

Summary: Household sentiment steady in March; second consecutive month of “extremely weak” readings; two consecutive readings below 80 in 1991, 1986; three of five sub-indices lower; more respondents expecting higher jobless rate.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment has deteriorated significantly over the past year, while business sentiment has been more robust.

According to the latest Westpac-Melbourne Institute survey conducted in the second week of March, household sentiment has steadied, albeit at a low level. Their Consumer Sentiment Index remained unchanged from February’s reading of 78.5, a reading which is well below the “normal” range and significantly lower than the long-term average reading of just over 101.

“This marks the second consecutive month of extremely weak consumer sentiment,” said Westpac Chief Economist Bill Evans. “Index reads below 80 are rare, back-to-back reads even rarer.”

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

Commonwealth Government bond yields fell significantly on the day following unusually large falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had shed 16bps to 3.05%, the 10-year yield had lost 7bps to 3.45% while the 20-year yield finished 3bps lower at 3.91%.

In the cash futures market, expectations regarding future rate rises over the next year softened considerably. At the end of the day, contracts implied the cash rate would remain essentially steady at the current rate of 3.57% to average 3.56% in April and May. August contracts implied a 3.505% average cash while November contracts implied 3.485%.

Evans noted the previous time two consecutive readings below 80 were printed was in the 1991 recession and before that, in 1986 when Australia lost its AAA credit rating.

Three of the five sub-indices registered lower readings, with the “Time to buy a major household item” sub-index again posting the largest monthly percentage loss.

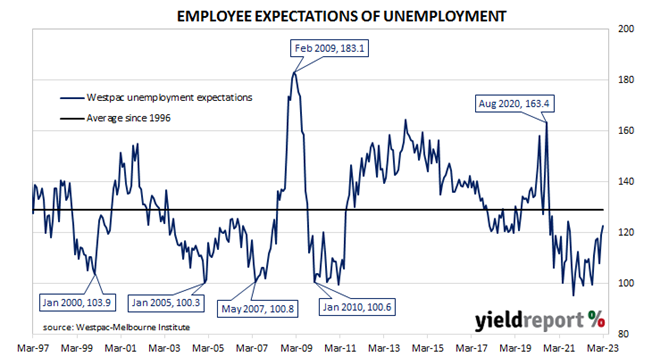

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, rose from 119.4 to 122.9. Higher readings result from more respondents expecting a higher unemployment rate in the year ahead.