Summary: No growth in private sector credit in April; business lending stalls; owner-occupier lending maintained; investor lending goes backwards faster; negative lending growth expected in 2021/22.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but the most recent numbers do not look promising.

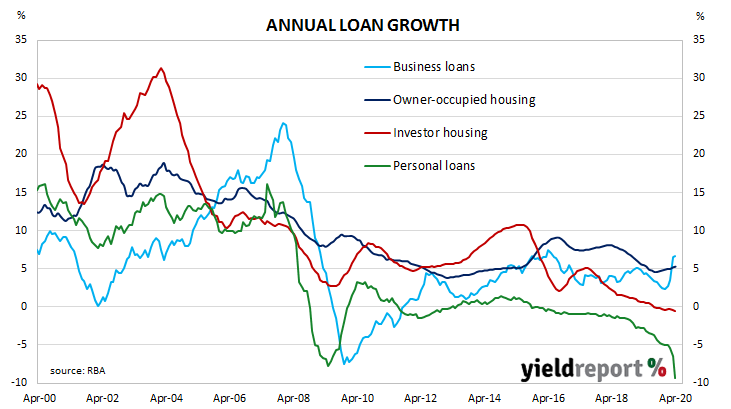

According to the latest RBA figures, private sector credit growth was zero in April. The result was well below the +0.6% increase which had been expected and considerably below March’s +1.1% increase. The annual growth rate slipped from March’s revised annual rate of 3.7% to 3.6%.

The flat result came about from a reduction in personal debt and investor housing loans in conjunction with a steady rise in owner-occupier loans. Business lending barely rose over the month.

After the March figures were released a month ago, ANZ economist Hayden Dimes had noted the increase had been driven by a jump in business credit which had not been that large since 1988. This month, business credit growth also played a significant role, just not in the same direction. “Credit growth slowed sharply in April as business credit growth came off. This sharp reversion in business credit growth likely means the precautionary shoring up of balance sheets seen in February and March is over.”

Local Treasury bonds yields moved modestly higher, just as US Treasury yields had in overnight trading. By the end of the Australian trading day, the 3-year Treasury bond yield remained unchanged at 0.27%, the 10-year yield had ticked up 1bp to 0.88% and the 20-year yield finished 2bps higher at 1.49%.

In the cash futures market, expectations of a rate cut softened. At the close of business, June contracts implied a rate cut down to zero as a 47% chance, down from the previous day’s 49%. July contracts implied a 57% chance of such a move, down from 59%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 35% and 48%.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.5% over the month, the same rate as in April. The sector’s 12-month growth rate ticked up to 5.3% in April from March’s rate of 5.2%.