Summary:

Australia’s $38.8 billion listed bank hybrid market is being wound down under an APRA-led phaseout, forcing investors into higher-risk assets in search of yield and potentially reshaping global regulatory attitudes toward hybrid instruments. The decision, unique in its scope, comes amid global reassessment following the Credit Suisse hybrid wipe-out in 2023, where Swiss authorities controversially wrote off US$17 billion of Additional Tier 1 securities—an action later ruled legally baseless by Switzerland’s Federal Administrative Court. That episode underscored the fragility of hybrids, which sit between debt and equity and can be written down or converted during crises.

APRA argues that retail ownership of hybrids could pose a political moral hazard—that the government might hesitate to enforce losses on “mum and dad” investors in a bank failure. Critics like Christopher Joye contend this logic is inconsistent, as retail investors hold far larger exposures in bank equities. Hybrids, he argues, are simpler and less volatile than shares, with predictable income streams and lower price risk. APRA’s move could paradoxically increase system risk, by removing a layer of contingent capital and boosting bank leverage.

The unwind will see a wave of redemptions, including $900 million in AMP and Macquarie hybrids by year-end and another $2.7 billion from Challenger, Suncorp, and NAB by June 2026. With yields compressed to pre-GFC levels—new five-year bank hybrids offering just 1.9% above BBSW, or roughly 3.8% cash yield—investors are being pushed toward subordinated debt, private credit, and structured convertible notes, all of which carry higher liquidity and credit risks.

Globally, regulators are also rethinking hybrid frameworks. New Zealand is considering replacing bank hybrids with subordinated bonds, while global banks are issuing hybrid-like instruments in Australian dollars to fill the gap. Meanwhile, private credit funds are exploiting the vacuum with high-yield listed notes.

Critics warn that APRA’s policy may have unintended consequences: by eliminating a vital capital buffer, it could make banks riskier and leave consumers chasing returns in less transparent, less liquid markets—a shift that benefits regulators more than investors.

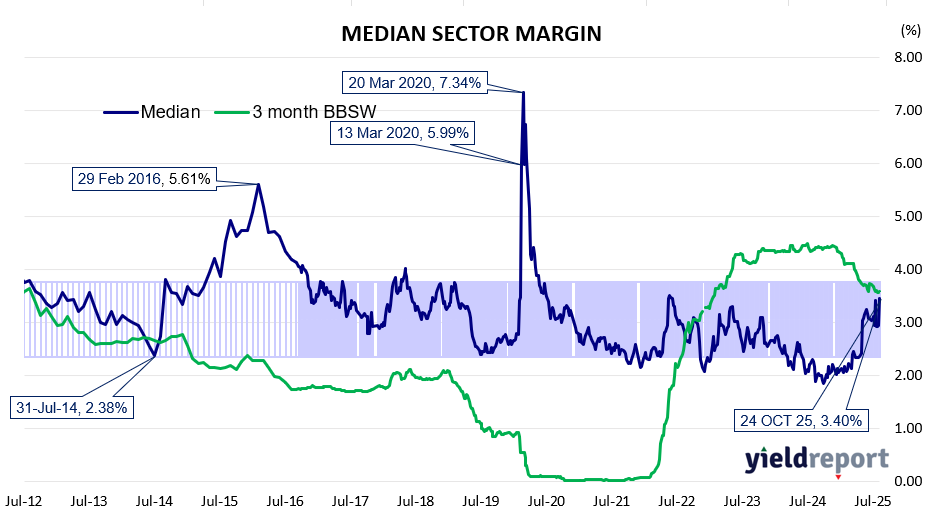

Figure 1: Hybrids: Median Sector Margin

ASX-Listed Hybrids

COMPANY CODE HYBRID TYPE MATURITY/

CALL

DATEISSUE MARGIN (inc frank) TRADING

MARGINDAY

CHANGEDAY

CLOSERUNNING

YIELD**AMP Group AMPPB Capital Notes 2 16/12/2025 4.50% 5.62% 1.16% 100.76 8.16% Macquarie Bank MBLPC Capital Notes 2 22/12/2025 4.70% 6.24% 0.17% 100.72 8.37% Challenger CGFPC Capital Notes 3 25/05/2026 4.60% 3.06% 0.05% 102.70 8.17% Nat Aust Bank NABPF Capital Notes 3 17/06/2026 4.00% 2.39% -0.04% 102.29 7.57% Suncorp SUNPH Capital Notes 3 17/06/2026 3.00% 2.80% 0.24% 101.27 6.64% Macquarie Group MQGPD Capital Notes 4 10/09/2026 4.15% 2.00% 0.03% 102.84 7.65% CBA CBAPJ PERLS 13 20/10/2026 2.75% 2.15% 0.59% 101.66 6.36% Latitude LFSPA Capital Notes 27/10/2026 4.75% 6.41% -0.95% 99.01 8.51% Westpac WBCPJ Capital Notes 7 22/03/2027 3.40% 1.96% -0.11% 103.03 6.91% CBA CBAPI PERLS 12 20/04/2027 3.00% 1.78% -0.20% 102.90 6.53% Bank of Queensland BOQPF Capital Notes 2 14/05/2027 3.80% 2.41% -0.10% 102.21 7.29% Bendigo Bank BENPH Capital Notes 15/06/2027 3.80% 2.55% 0.14% 103.31 7.30% Macquarie Group MQGPE Capital Notes 5 20/09/2027 2.90% 2.36% 0.34% 101.86 6.48% Nat Aust Bank NABPH Capital Notes 5 17/12/2027 3.50% 2.08% -0.01% 104.14 6.94% ANZ Bank AN3PI Capital Notes 6 20/03/2028 3.00% 1.80% -0.14% 103.50 6.47% CBA CBAPL PERLS 15 15/06/2028 2.85% 1.74% 0.02% 103.89 6.32% Suncorp SUNPI Capital Notes 4 17/06/2028 2.90% 2.03% -0.30% 103.34 6.40% Westpac WBCPL Capital Notes 9 22/09/2028 3.40% 1.97% -0.05% 104.96 6.78% Macquarie Bank MBLPD Capital Notes 3 7/12/2028 2.90% 2.11% 0.08% 103.30 6.40% Bank of Queensland BOQPG Capital Notes 3 15/12/2028 3.40% 2.47% 0.35% 104.08 6.85% Judo Capital JDOPA Capital Notes 16/02/2029 6.50% 3.31% -0.04% 112.19 9.24% ANZ Bank AN3PJ Capital Notes 7 20/03/2029 2.70% 1.70% -0.22% 103.87 6.15% Challenger CGFPD Capital Notes 4 25/05/2029 3.60% 2.42% 0.15% 105.50 6.97% CBA CBAPK PERLS 14 15/06/2029 2.75% 1.89% -0.15% 103.97 6.21% Insurance Australia IAGPE Capital Notes 2 15/06/2029 3.50% 2.14% -0.12% 105.38 6.84% Macquarie Group MQGPF Capital Notes 6 12/09/2029 3.70% 2.24% 0.02% 106.10 6.99% Nat Aust Bank NABPI Capital Notes 6 17/09/2029 3.15% 1.89% 0.06% 105.60 6.50% Westpac WBCPK Capital Notes 8 21/09/2029 2.90% 2.05% 0.08% 104.00 6.35% ANZ Bank AN3PK Capital Notes 8 20/03/2030 2.75% 1.97% 0.07% 103.80 6.20% CBA CBAPM PERLS 16 17/06/2030 3.00% 1.89% -0.09% 105.65 6.36% Suncorp SUNPJ Capital Notes 5 17/06/2030 2.80% 2.21% -0.15% 103.60 6.29% Nat Aust Bank NABPJ Capital Notes 7 17/09/2030 2.80% 2.02% -0.06% 104.46 6.23% Bendigo Bank BENPI Capital Notes 2 13/12/2030 3.20% 2.20% -0.04% 105.60 6.55% Insurance Australia IAGPF Capital Notes 3 15/12/2030 3.20% 2.09% -0.22% 105.74 6.53% ANZ Bank AN3PL Capital Notes 9 20/03/2031 2.90% 1.93% 0.06% 105.20 6.26% Westpac WBCPM Capital Notes 10 22/09/2031 3.10% 1.99% -0.09% 106.50 6.39% Macquarie Group MQGPG Capital Notes 7 15/12/2031 2.65% 2.19% 0.04% 103.32 6.14% Nat Aust Bank NABPK Capital Notes 8 17/03/2032 2.60% 1.83% -0.11% 105.19 6.00% ASX-Listed Hybrids (Non-standard)

COMPANY CODE BOND TYPE CALL DATE ISSUE MARGIN (inc frank) TRADING MARGIN DAY CLOSING PRICE RUNNING YIELD Nufarm NFNG Step Up Perpetual 3.90% 5.30% 0.01% 87.5 8.95% Ramsay Health Care RHCPA Preference Share Perpetual 4.85% 4.64% 0.05% 106.19 8.29%