Summary:

Swap rates showed mixed movements across short- and long-term maturities. Short-term swaps (1–6 months) were mostly flat to slightly lower over the month, with the 1-month rate at 3.66% (-0.11% monthly) and the 6-month rate at 3.75% (-0.03% monthly). Medium- to long-term swaps (1–15 years) edged higher both weekly and monthly, reflecting modest upward pressure on longer-dated rates. The 1-year rate was 3.37% (+0.03% monthly), while the 10- and 15-year rates rose to 4.24% and 4.49%, up 0.11% and 0.12% over the month, respectively. Overall, short-term stability contrasted with gradual long-term increases.

For the week ending 29th August 2025, the 1-month BBSW held at 3.56% (flat), while the 3-month BBSW closed at 3.56% (flat), based on daily data trends. The 6-month BBSW was also flat at 3.66, reflecting lack of any interest rate-sensitive news and neutral market sentiment towards short-term rate expectations.

The longer end of the swap rate curve also remains steady over the week, with the 1-year swap rate up 2 basis points to 3.32%. The 3-year swap rate increased 3 basis points to end the week at 3.32%. The 5-year swap rate increased 6 basis points to 3.72%, reflecting investor expectations ofa revised cash rate path for Australia following the RBA’s highly anticipated rate cut amid slowing domestic growth and uncertainties around US tariffs.

Bank Bill Swap Rates

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 month 3.66 0 -0.11 3 months 3.66 0.02 -0.08 6 months 3.75 0.06 -0.03 SWAP RATES

TERM TO MATURITY CLOSING RATE Δ WEEK Δ MONTH 1 year 3.37 0.04 0.03 3 years 3.39 0.07 0.1 5 years 3.79 0.07 0.11 10 years 4.24 0.06 0.11 15 years 4.49 0.05 0.12

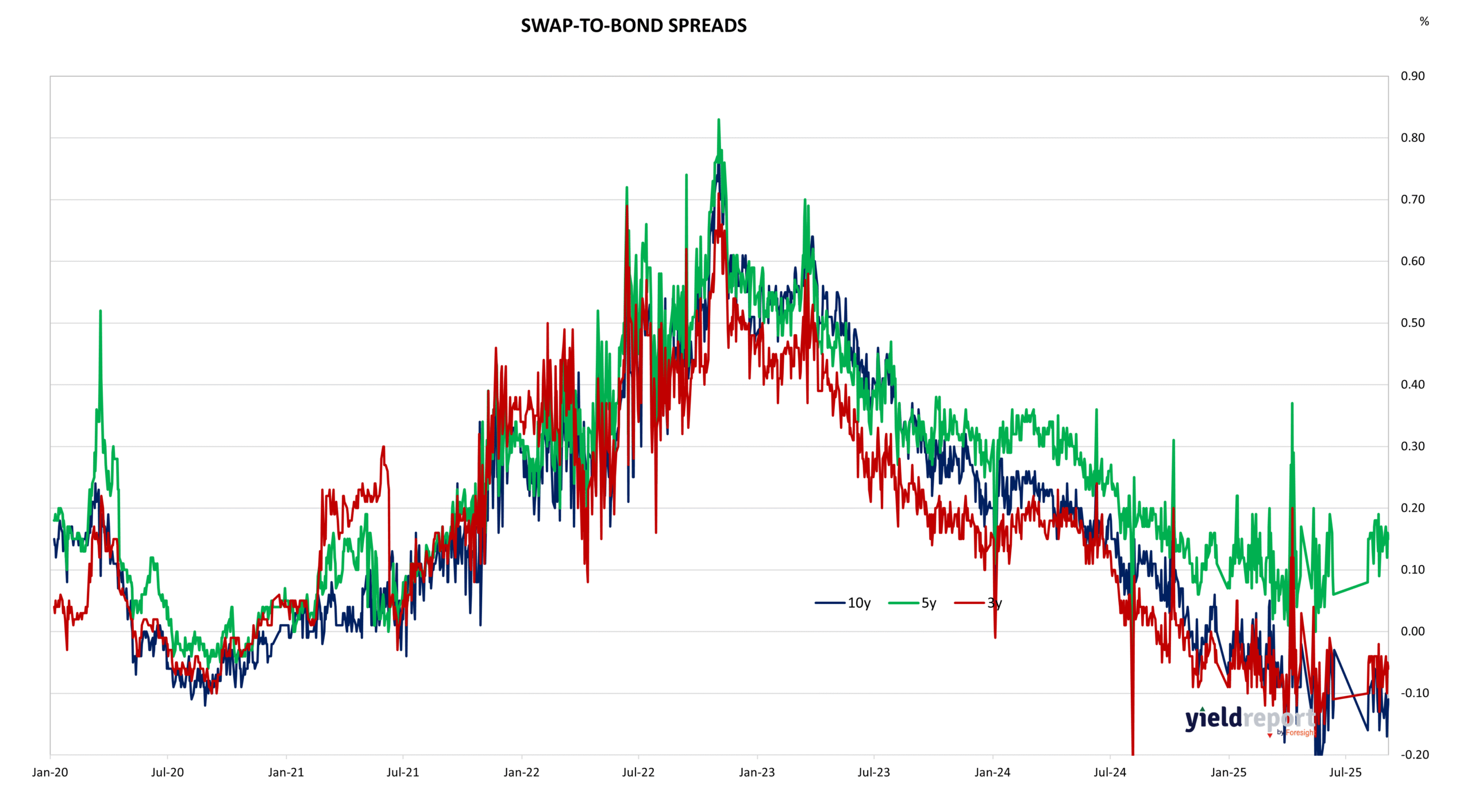

Exhibit 1: Australian 3Y/10Y Bond Yield