The physical bank bill rate and 3 month BBSW both fell by 5bps to 2.06%.

In its monetary policy decision statement, the RBA made another reference to “short-term wholesale interest rates”. They described increases in recent months as “partly due to developments in the United States, but there are other factors at work as well. It remains to be seen the extent to which these factors persist.” In their view, higher BBSW rates are not just a function of higher USD LIBOR rates.

Swap rates generally tracked their Commonwealth benchmarks quite well. The 1 year rate slipped 1 bp to 2.02%, the 3 year rate remained unchanged at 2.16%, 5 year rates slipped 1bp to 2.49%, the 10 year rate lost 2bps to 2.82% and the 15 year rate fell by 3bps to 2.98%.

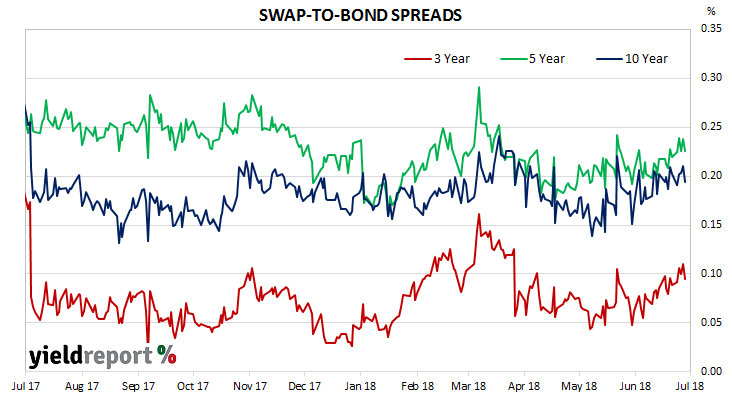

As a result, swap-to-bond spreads barely changed; the 3 year spread remained at 9bps while the 5 year spread added 1bp to 23bps and the 10 year spread slipped 1bp to 19bps.

AFMA BBSW - SWAP RATES

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 1.98 | -0.04 | 0.13 |

| 90 Day | 2.06 | -0.05 | 0.12 |

| 180 Day | 2.18 | -0.04 | 0.12 |

| 1 Year | 2.02 | -0.01 | 0.06 |

| 3 Year | 2.16 | 0.00 | -0.07 |

| 5 Year | 2.49 | -0.01 | -0.12 |

| 10 Year | 2.82 | -0.02 | -0.14 |

| 15 Year | 2.98 | -0.03 | -0.17 |