The physical bank bill rate and the 3 month BBSW both increased by 3bps to 2.03%. Both rates are now at a 53bps margin to the official cash rate. There has been quite a bit of commentary on the gap between BBSW and the cash rate/OIS recently. One explanation from a very senior economist is the increase in the spread is a symptom of a short-term lack of available funds rather than some sort of comment on bank risk.

The gradient of the government bond yield curve flattened as yields at the long end fell a little more than those at the short end. Swap rates moved in a broadly similar manner. The 1 year swap slipped by 1bp to 1.95%, 3 year rates lost 4bps to 2.17%, the 5 year swap rate fell by 5bps to 2.52%, the 10 year lost 4bps to 2.82% and the 15 year rate fell by 5bps to 2.99%.

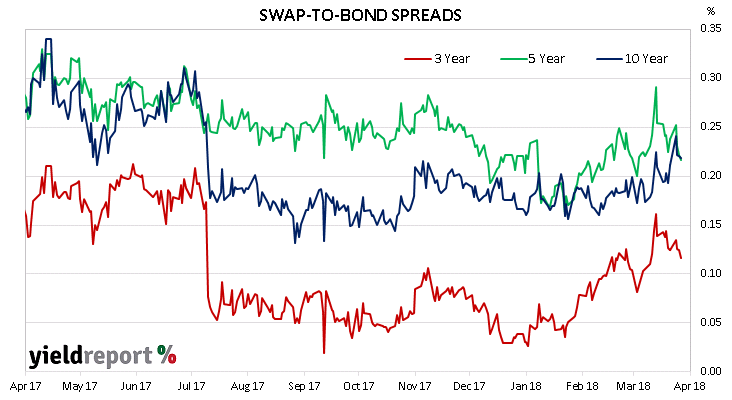

As a result, movements in swap-to-bond spreads did not follow a common path. The 3 year spread remained unchanged at 12bps, the 5 year spread tightened by 2bps to 22bps and the 10 year spread added 1bp to 22bps.

AFMA BBSW - SWAP RATES

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 1.83 | 0.03 | 0.16 |

| 90 Day | 2.03 | 0.03 | 0.27 |

| 180 Day | 2.12 | 0.01 | 0.20 |

| 1 Year | 1.95 | -0.01 | 0.09 |

| 3 Year | 2.17 | -0.04 | -0.06 |

| 5 Year | 2.52 | -0.05 | -0.14 |

| 10 Year | 2.82 | -0.04 | -0.26 |

| 15 Year | 2.99 | -0.05 | -0.31 |