The physical bank bill rate and 3 month BBSW both fell back by 3bps to 2.02%.

The gradient of the government bond yield curve flattened a little as yields fell across the curve. Swap rates largely tracked their Commonwealth benchmarks with some variance at the front and end of the curve.

The 1 year swap slipped 1bp to 2.02%, the 3 year rate lost 4bps to 2.25%, 5 year rates fell by 5bps to 2.61% and both 10 year and 15 year rates decreased by 7bps to 2.93% and 3.11%.

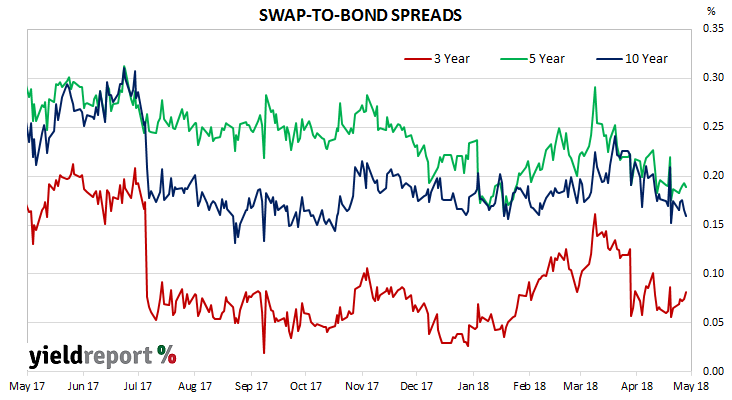

As a result, swap-to-bond spreads widened at the short end but contracted at the long end. The 3 year spread increased by 2bps to 8bps, the 5 year spread remained unchanged at 19bps and the 10 year spread gave back 2bps to 16bps.

AFMA BBSW - SWAP RATES

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 1.89 | -0.01 | 0.09 |

| 90 Day | 2.02 | -0.03 | 0.02 |

| 180 Day | 2.11 | -0.04 | 0.00 |

| 1 Year | 2.02 | -0.01 | 0.06 |

| 3 Year | 2.25 | -0.04 | 0.04 |

| 5 Year | 2.61 | -0.05 | 0.04 |

| 10 Year | 2.93 | -0.07 | 0.07 |

| 15 Year | 3.11 | -0.07 | 0.07 |