Summary: 3-month steady at 0.02%, 6-month BBSW up 1bp to 0.05%; swap rates higher across curve; swap spreads wider.

3-month BBSW remained unchanged at 0.02% while 6-month BBSW inched up 1bp to 0.05%.

Swap rates rose by increasing amounts along the curve. By the end of the week, the 1-year rate had crept up 1bp to 0.06%, the 3-year rate had added 4bps to 0.51%, the 5-year rate had gained 7bps to 0.99%, the 10-year rate had increased by 12bps to 1.64% while the 15-year rate finished 11bps higher at 1.92%.

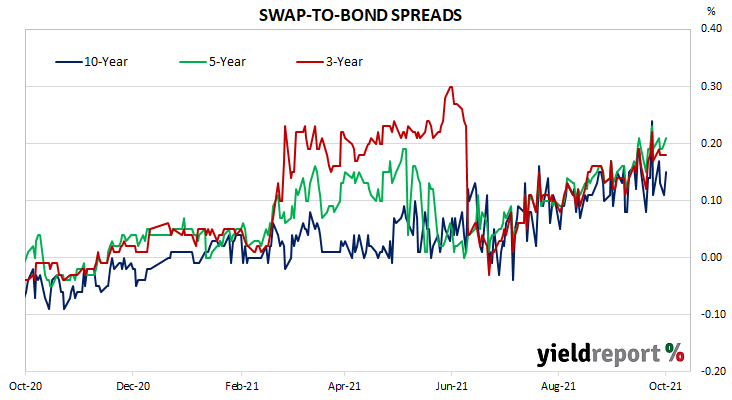

As a result, swap spreads were pretty stable except at the long end. By the end of the week, the 3-year spread had ticked up 1bp to 18bps, the 5-year spread had gained 2bps to 21bps while the 10-year spread finished 4bps higher at 15bps.

NB. Spreads are calculated with respect to “spot” Australian Commonwealth Government bond yields.

BBSW - SWAP RATES

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 0.00 | -0.01 | 0.00 |

| 90 Day | 0.02 | 0.00 | 0.01 |

| 180 Day | 0.05 | 0.01 | 0.02 |

| 1 Year | 0.06 | 0.01 | 0.02 |

| 3 Year | 0.51 | 0.04 | 0.09 |

| 5 Year | 0.99 | 0.07 | 0.20 |

| 10 Year | 1.64 | 0.12 | 0.27 |

| 15 Year | 1.92 | 0.11 | 0.28 |